3 Asian Stocks Estimated To Be Trading Below Intrinsic Value By Up To 48.3%

As global markets grapple with inflation pressures and geopolitical uncertainties, Asian equities present a compelling narrative amidst these broader economic challenges. In this environment, identifying undervalued stocks can be particularly advantageous, as they may offer potential value relative to their intrinsic worth despite the prevailing market volatility.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Strike Group (TSE:6196) | ¥1205.00 | ¥2386.66 | 49.5% |

| Plus Alpha ConsultingLtd (TSE:4071) | ¥2392.00 | ¥4709.96 | 49.2% |

| Peijia Medical (SEHK:9996) | HK$5.21 | HK$10.14 | 48.6% |

| LianChuang Electronic TechnologyLtd (SZSE:002036) | CN¥8.51 | CN¥16.95 | 49.8% |

| GenFleet Therapeutics (Shanghai) (SEHK:2595) | HK$36.40 | HK$71.19 | 48.9% |

| freee K.K (TSE:4478) | ¥2199.00 | ¥4349.05 | 49.4% |

| Cybozu (TSE:4776) | ¥2452.00 | ¥4871.58 | 49.7% |

| Beijing Luzhu Biotechnology (SEHK:2480) | HK$19.70 | HK$39.40 | 50% |

| BEAUTY GARAGE (TSE:3180) | ¥1418.00 | ¥2827.79 | 49.9% |

| Auras Technology (TPEX:3324) | NT$939.00 | NT$1836.82 | 48.9% |

We're going to check out a few of the best picks from our screener tool.

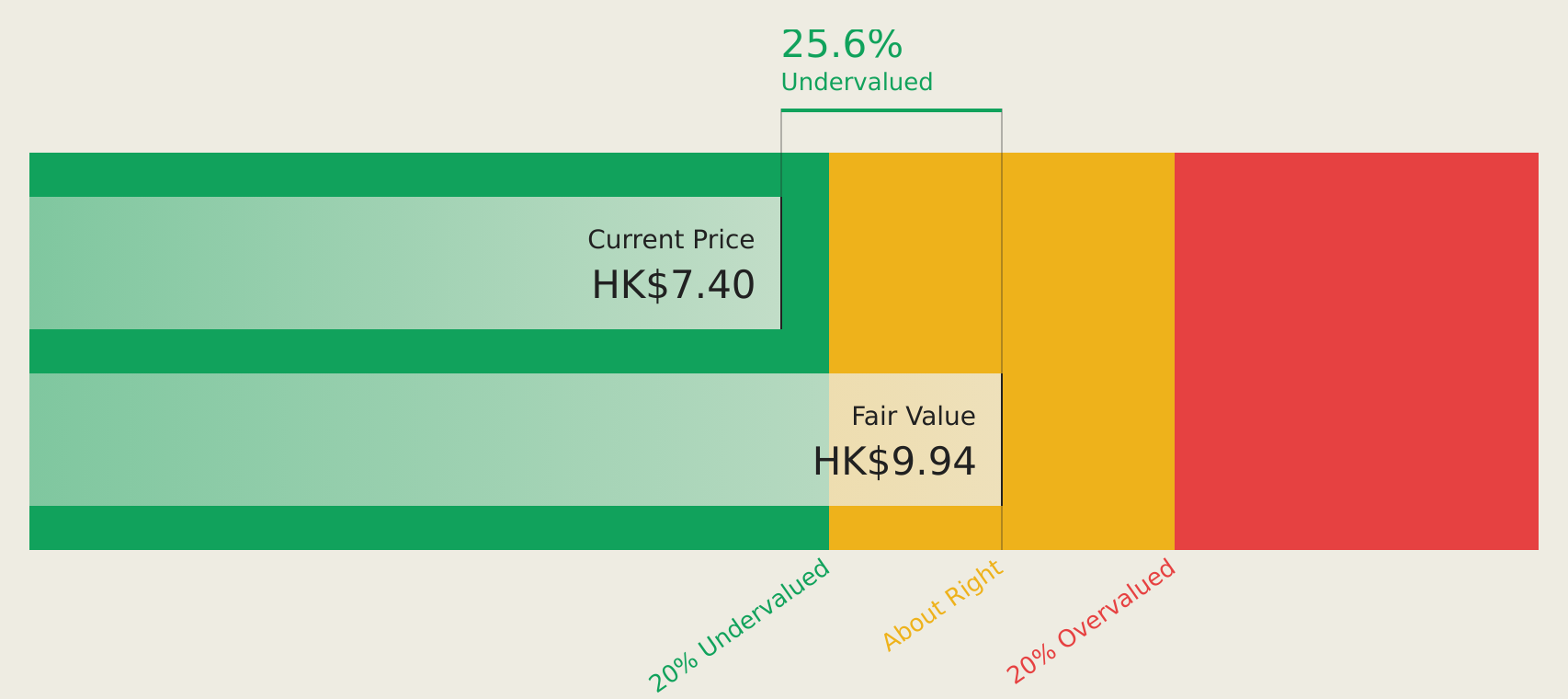

MicroTech Medical (Hangzhou) (SEHK:2235)

Overview: MicroTech Medical (Hangzhou) Co., Ltd. specializes in diabetes management, treatment, and monitoring medical devices both in China and internationally, with a market cap of HK$3.35 billion.

Operations: The company generates revenue of CN¥660.79 million from its research and development, manufacture, and sales of medical devices.

Estimated Discount To Fair Value: 19%

MicroTech Medical (Hangzhou) is trading at HK$8.04, below its estimated future cash flow value of HK$9.93, indicating potential undervaluation. The company reported a significant turnaround with net income reaching CNY 40.15 million from a loss the previous year and sales increasing to CNY 660.79 million, driven by strong performance in continuous glucose monitoring systems and international market expansion. Earnings are expected to grow significantly at 44.91% annually, outpacing the Hong Kong market's growth rate.

- In light of our recent growth report, it seems possible that MicroTech Medical (Hangzhou)'s financial performance will exceed current levels.

- Dive into the specifics of MicroTech Medical (Hangzhou) here with our thorough financial health report.

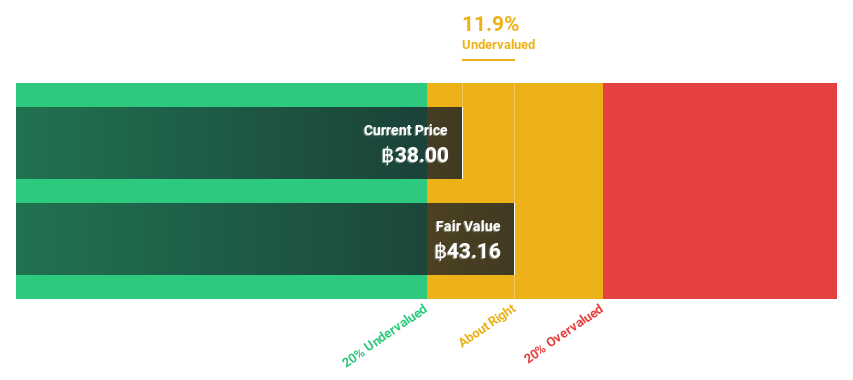

Moshi Moshi Retail Corporation (SET:MOSHI)

Overview: Moshi Moshi Retail Corporation Public Company Limited operates in Thailand, focusing on the retail and wholesale of lifestyle products, with a market capitalization of THB11.96 billion.

Operations: The company's revenue segments include retail sales of THB2.45 billion and wholesale operations generating THB1.78 billion.

Estimated Discount To Fair Value: 48.3%

Moshi Moshi Retail Corporation, trading at THB36.25, is valued below its estimated future cash flow value of THB70.06, presenting a potential undervaluation opportunity. Recent earnings for Q1 2026 showed sales of THB 984.41 million and net income of THB 190.99 million, both up from the previous year. With earnings forecast to grow at 13.9% annually and revenue expected to outpace the Thai market growth rate, it offers promising prospects despite moderate growth expectations.

- Our growth report here indicates Moshi Moshi Retail Corporation may be poised for an improving outlook.

- Click to explore a detailed breakdown of our findings in Moshi Moshi Retail Corporation's balance sheet health report.

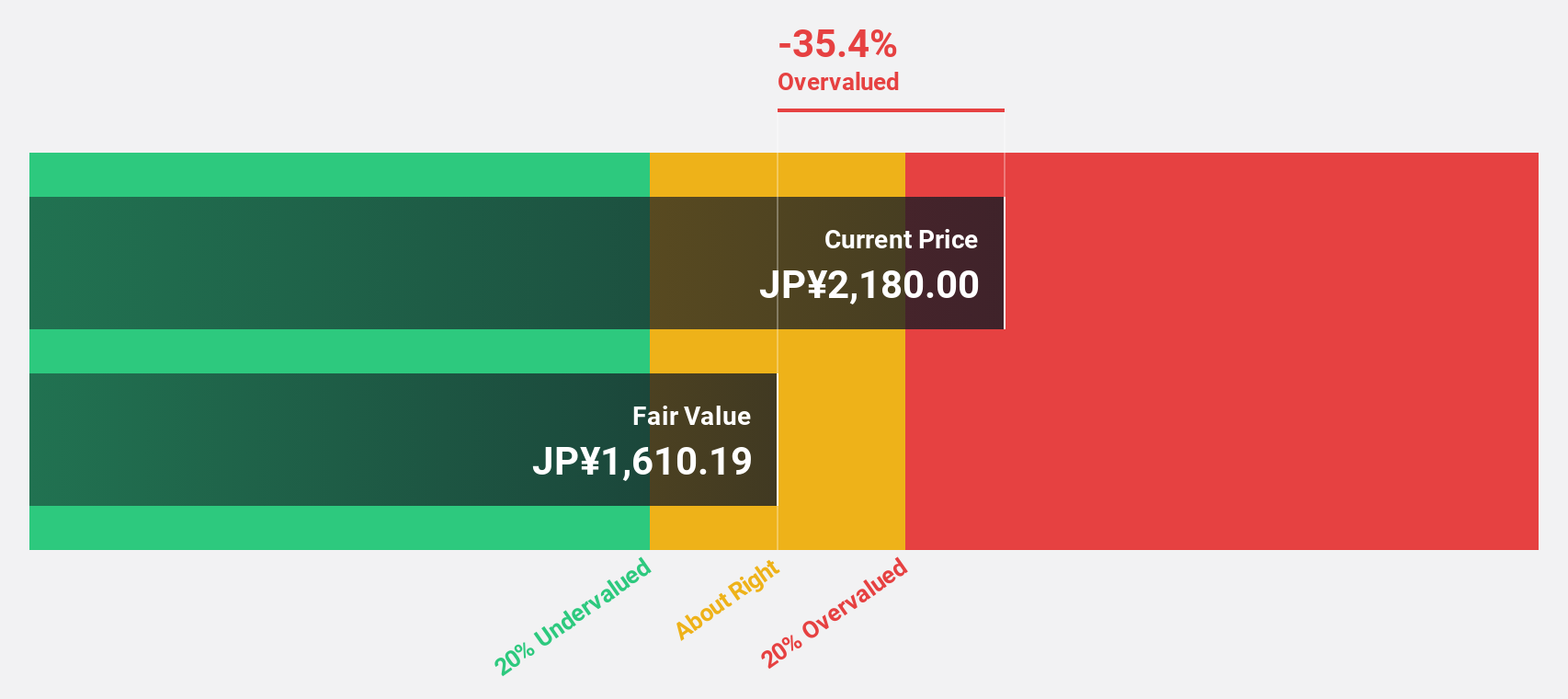

Premium Group (TSE:7199)

Overview: Premium Group Co., Ltd. provides financing and services globally with a market cap of ¥77.32 billion.

Operations: The company generates revenue through its Finance segment (¥25.39 billion), Automobile Warranty services (¥8.06 billion), and Automobility Service, including the Car Premium Business (¥13.19 billion).

Estimated Discount To Fair Value: 48.3%

Premium Group, priced at ¥1989, is trading significantly below its estimated future cash flow value of ¥3850.14. The company reported a rise in annual sales to ¥44.04 billion and net income to ¥6.07 billion for the fiscal year ending March 2026. Despite dividends not being fully covered by free cash flows, earnings are projected to grow faster than the Japanese market at 14.8% per year, supported by strong recent profit growth of 30.5%.

- Insights from our recent growth report point to a promising forecast for Premium Group's business outlook.

- Navigate through the intricacies of Premium Group with our comprehensive financial health report here.

Make It Happen

- Investigate our full lineup of 196 Undervalued Asian Stocks Based On Cash Flows right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English