FTAI Aviation (FTAI) Is Up 6.0% After Oversubscribed Inaugural Aircraft Lease ABS Deal Pricing

- FTAI Aviation recently priced its inaugural aircraft lease asset-backed securitization, MRE 2026-1, a US$612.0 million deal backed by 48 on-lease narrowbody aircraft serving 23 airlines worldwide.

- The strong oversubscription of the transaction highlights investor confidence in FTAI’s aircraft leasing platform and its broader shift toward diversified, capital-markets-based funding.

- Next, we’ll examine how this oversubscribed aircraft ABS issuance could reshape FTAI Aviation’s investment narrative and long-term financing profile.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

FTAI Aviation Investment Narrative Recap

To own FTAI Aviation, you have to believe its focus on midlife engines, aircraft leasing, and capital light structures can keep generating attractive economics despite concentration in legacy platforms. The oversubscribed US$612.0 million aircraft ABS supports that thesis but does not remove the key near term swing factors: successful scaling of the SCI model on one side, and the risk that demand for CFM56 and other legacy engines fades faster than expected on the other.

The news that FTAI will redeem all outstanding 8.25 percent Series C preferred shares at US$25.00 per share fits with this shift toward a more flexible, capital markets driven balance sheet. Taken together with the new ABS, it reinforces how the company is retooling its funding mix around cheaper, diversified sources, which could matter a lot if engine aftermarket demand or SCI partner appetite ever falls short of expectations.

Yet while the funding story looks strong, investors should still watch how exposed FTAI is if airlines accelerate away from older engine platforms and...

Read the full narrative on FTAI Aviation (it's free!)

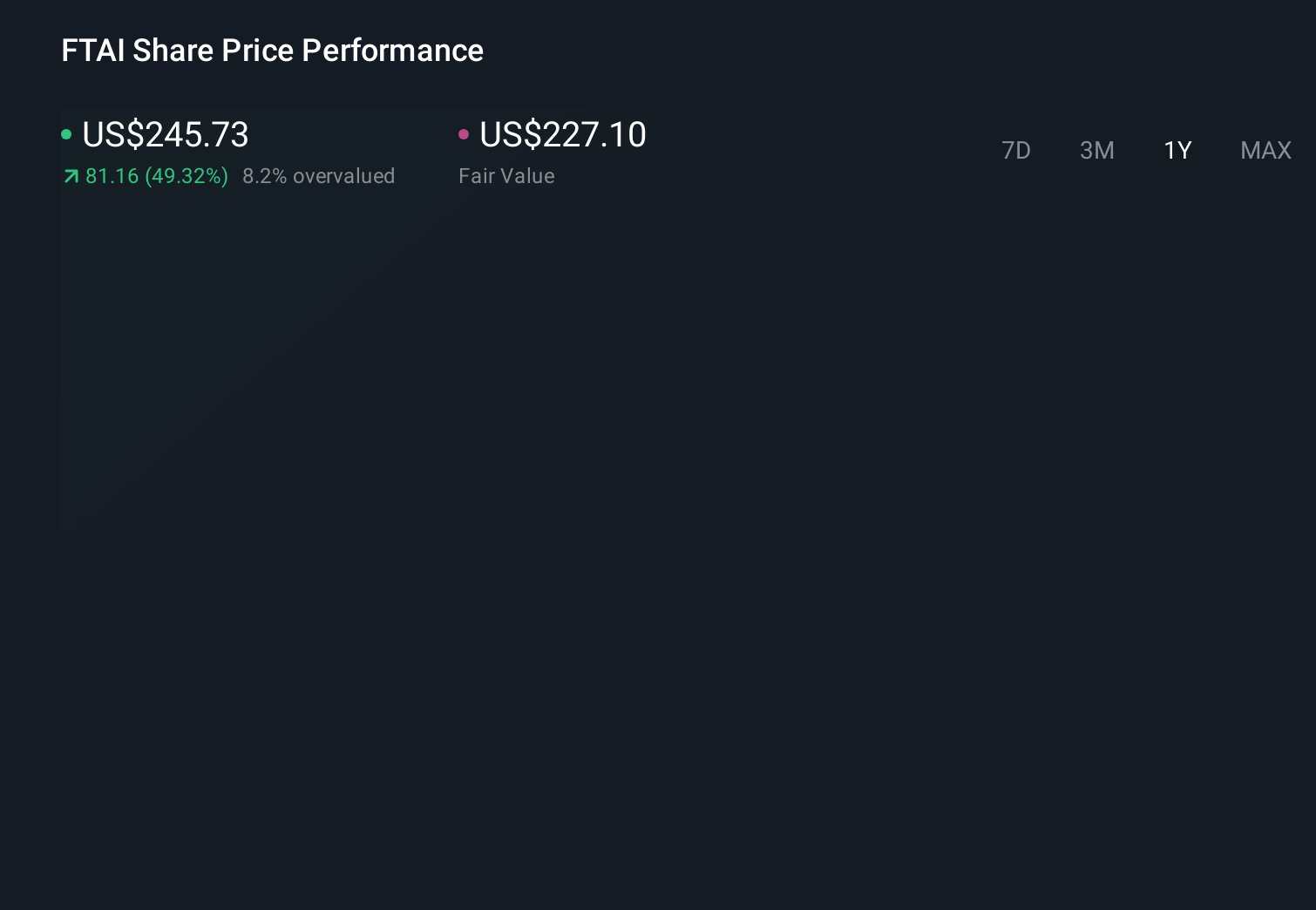

FTAI Aviation's narrative projects $6.6 billion revenue and $1.7 billion earnings by 2029. This requires 32.8% yearly revenue growth and about a $1.2 billion earnings increase from $521.7 million today.

Uncover how FTAI Aviation's forecasts yield a $350.60 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming roughly US$4.6 billion of revenue and US$1.3 billion of earnings by 2029, yet they still framed FTAI’s concentration in legacy engines as a major overhang, reminding you that even with this ABS milestone, opinions on future risk and reward can differ widely and may shift again as new information comes through.

Explore 5 other fair value estimates on FTAI Aviation - why the stock might be worth just $245.03!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FTAI Aviation research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free FTAI Aviation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FTAI Aviation's overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English