Should Brookdale’s Stronger 2026 EBITDA Outlook and Occupancy Momentum Reframe the BKD Turnaround Narrative?

- Brookdale Senior Living recently presented at the Bank of America Global Healthcare Conference in Las Vegas and the RBC Capital Markets Global Healthcare Conference in New York, highlighting its latest operational and financial updates.

- These appearances, coupled with management’s emphasis on rising occupancy, operational improvements, and double-digit 2026 EBITDA growth guidance, have reinforced market attention on Brookdale’s evolving business trajectory and leadership execution.

- Now, we’ll explore how Brookdale’s improved occupancy trends and stronger 2026 EBITDA guidance could influence the company’s existing investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Brookdale Senior Living Investment Narrative Recap

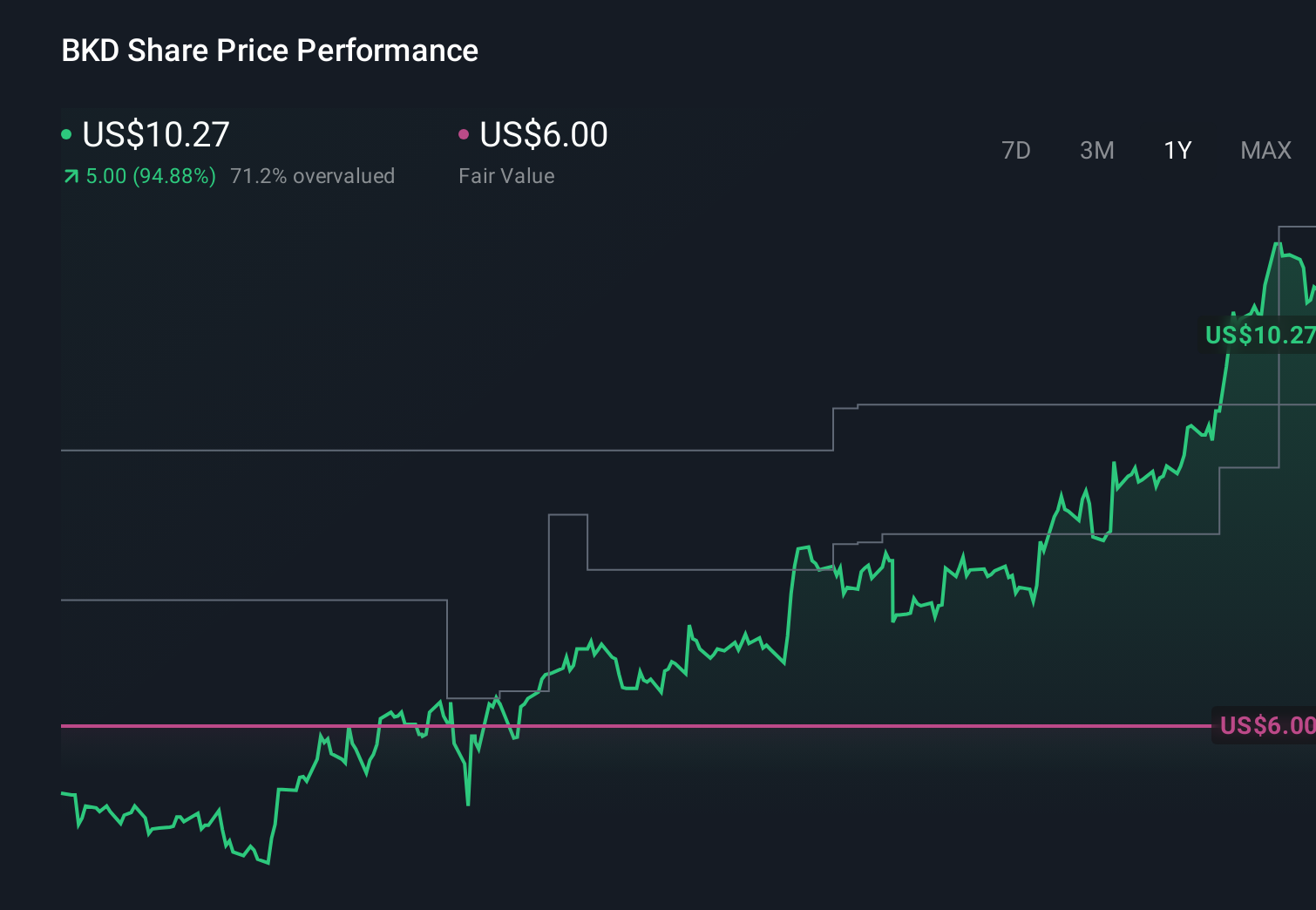

To own Brookdale today, you need to believe that improving occupancy and tighter operations can eventually outweigh ongoing losses, high leverage, and heavy capital needs. The recent conference presentations largely reinforce the near term catalyst of rising occupancy and management’s 2026 double digit EBITDA growth guidance, but they do not materially change the biggest current risk, which is whether higher labor and financing costs will keep eating into those operational gains.

The most relevant recent announcement here is Brookdale’s reaffirmed outlook for double digit EBITDA growth in 2026, supported by rising occupancy and pricing discipline. This ties directly into the key catalyst of operational leverage: with Q1 2026 occupancy around 82 percent and year on year gains continuing, management is effectively telling investors that incremental occupancy and rate improvements are expected to flow more meaningfully into EBITDA, even as the company remains loss making today.

Yet, against these encouraging updates, investors should still be aware of rising labor costs and refinancing risk, especially if occupancy momentum slows...

Read the full narrative on Brookdale Senior Living (it's free!)

Brookdale Senior Living's narrative projects $3.2 billion revenue and $104.8 million earnings by 2029. This requires 2.4% yearly revenue growth and a $309.4 million earnings increase from -$204.6 million today.

Uncover how Brookdale Senior Living's forecasts yield a $19.10 fair value, a 44% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady occupancy gains, the most optimistic analysts saw revenue reaching about US$3.3 billion and earnings of roughly US$175.8 million, which shows how far views can stretch and how recent guidance and conference commentary might push some of those expectations higher or lower over time.

Explore 2 other fair value estimates on Brookdale Senior Living - why the stock might be worth just $17.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Brookdale Senior Living research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Brookdale Senior Living research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brookdale Senior Living's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English