Assessing Talen Energy (TLN) Valuation After A Sharp 23.7% Weekly Share Price Move

Talen Energy (TLN) has drawn fresh attention after its stock moved 4.4% higher in the latest session and 23.7% over the past week, prompting investors to reassess the independent power producer’s recent fundamentals.

See our latest analysis for Talen Energy.

That sharp 23.7% 7 day share price return comes after a softer period, with the 90 day share price return slightly down 0.6% and the year to date share price return down 2.0%. The 1 year total shareholder return stands at 58.6%, suggesting momentum has picked up recently.

If recent gains in Talen Energy have you thinking about other power related ideas, this could be a good time to scan 35 power grid technology and infrastructure stocks

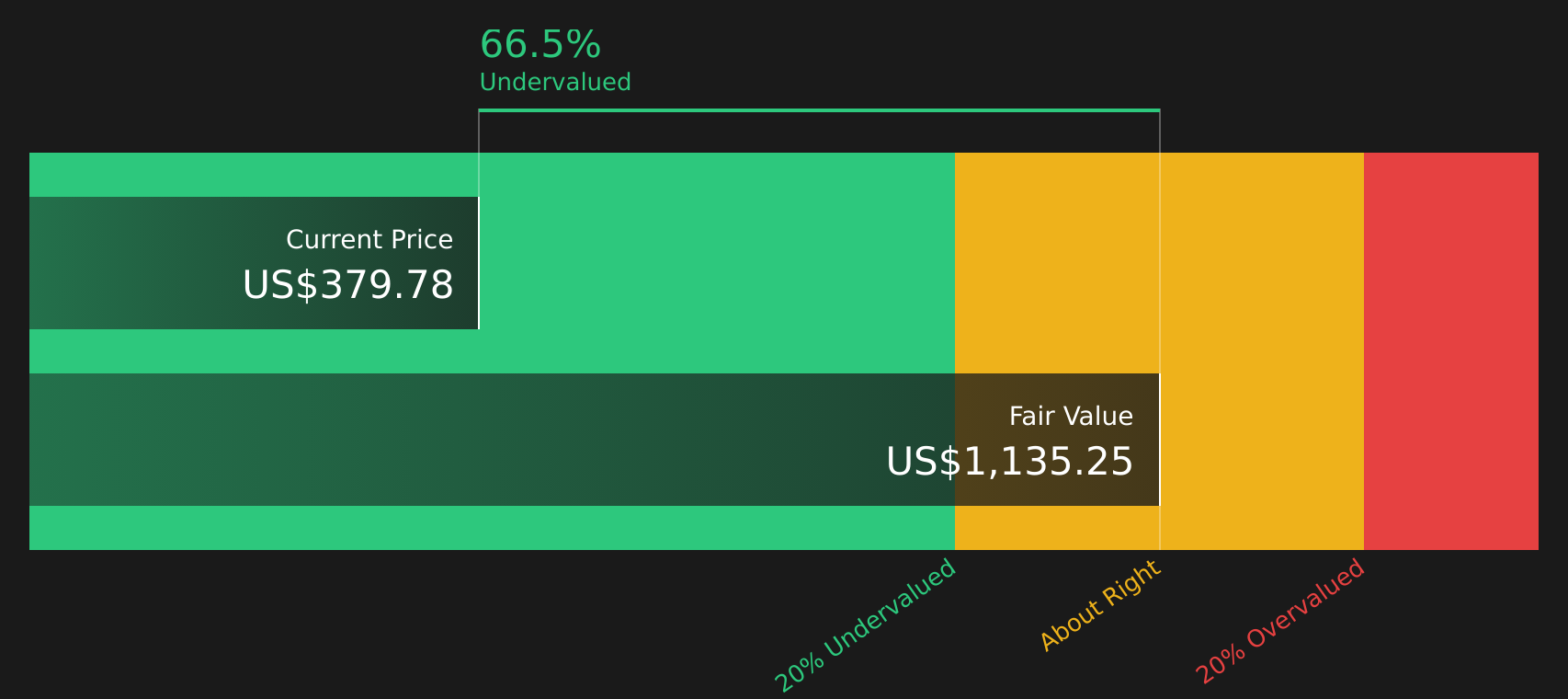

With the stock up 58.6% over the past year, yet still showing an estimated 65.9% intrinsic discount and trading below analyst price targets, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 17.2% Undervalued

At a last close of $389, the most widely followed narrative points to a fair value of about $469.57, framing Talen Energy as materially undervalued on that basis.

The acquisition and integration of new, highly efficient, low-carbon CCGT plants in key data center growth markets (Freedom and Guernsey) not only meet the accelerating load from electrification but are projected to deliver significant free cash flow per share accretion and support deleveraging, driving higher net margins.

Want to see what sits behind that cash flow story and margin lift? The narrative leans heavily on faster top line expansion, sharply higher profitability, and a richer earnings multiple embedded in its fair value math.

Result: Fair Value of $469.57 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to factor in Talen’s dependence on fossil fuel generation and its elevated debt from recent acquisitions, both of which could pressure future earnings and cash flows.

Find out about the key risks to this Talen Energy narrative.

Another Angle on Valuation

The earlier view leans heavily on discounted cash flows, with our model suggesting Talen Energy trades at about a 65.9% discount to an estimated $1,140.83 fair value, which points to a very undervalued setup. The open question is whether those cash flow assumptions prove conservative or too optimistic.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Uncertain about whether the recent data points justify the excitement or the caution, but ready to form your own view quickly by weighing both sides of the story, including the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with just one stock; use this momentum to line up a watchlist of quality candidates that fit different roles in your portfolio.

- Target potential mispricings by scanning carefully selected opportunities through the 46 high quality undervalued stocks.

- Strengthen your core holdings by focusing on companies screened in the solid balance sheet and fundamentals stocks screener (46 results).

- Get ahead of the crowd by reviewing underfollowed opportunities inside the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English