Is the Cheapest Cruise Line Stock Finally Too Cheap to Ignore?

Key Points

Norwegian Cruise Line CEO John Chidsey bought $2.5 million worth of his company's stock late last week.

The country's third-largest cruise line stock has been a historical laggard to the industry in more ways than one.

Even after a rough quarter led to a guidance reduction, NCL is trading for just 8 times next year's profit target.

Is the captain of Norwegian Cruise Line (NYSE: NCLH) signaling smooth sailing for the cruising industry's worst performer? CEO John Chidsey recently bought 153,000 shares of the weather-worn cruise line operator, investing roughly $2.5 million in his own company on Friday of last week.

As seasoned investors know, there are plenty of acceptable reasons for an insider to lighten a position. Executives might need to raise money. It could also be just part of the portfolio diversification process. However, there is usually only one reason for insider buying.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Is Chidsey signaling that Norwegian Cruise Line -- or NCL, for short -- has bottomed out? Let's take a closer look at the market's ugliest major cruise line operator.

Image source: Getty Images.

Taking on water

NCL stock has had a challenging month and year. With the general market clawing higher in May, at least 14 analysts have slashed their price targets on the country's third-largest publicly traded cruise line operator. There was also one outright downgrade.

The markdowns are fair. NCL issued a disappointing financial update on May 4. The first quarter itself was mixed but solid. Adjusted earnings more than doubled, giving the cruise line operator its biggest bottom-line beat in more than a year. Revenue rose 10%, just shy of what analysts were targeting, but still a reasonable offset to the bottom-line win.

The problem was guidance. With rising fuel costs jacking up operating costs and the war in Iran eating away at future bookings, NCL hosed down its full-year earnings guidance. Even with the monster beat, it now expects to earn between $1.45 and $1.70 per share on an adjusted basis for all of 2026. Earlier this year, it was modeling adjusted net income of $2.38 a share.

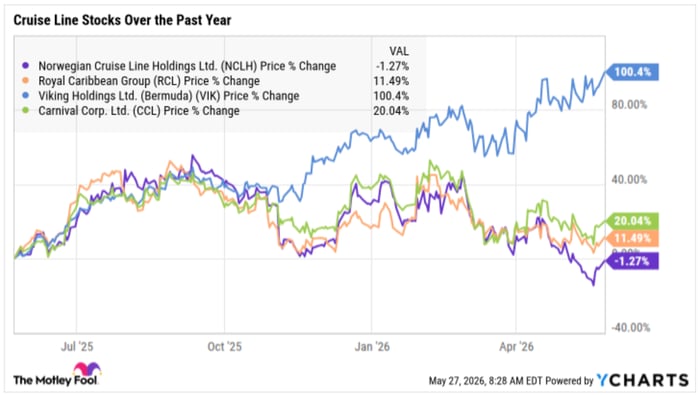

NCL stock is down 6% in May and trading 23% lower year to date. The stock's 1% decline over the past year may not seem so bad until you consider that larger rivals Carnival (NYSE: CCL) and Royal Caribbean (NYSE: RCL) have delivered double-digit gains over the same period. River cruise leader Viking Holdings (NYSE: VIK) has now officially doubled.

The industry is cruising. NCL has been moving in the opposite direction.

Coming up for air

The silver lining for the bronze medalist among the three mainstream ocean liners is that NCL trades at the lowest forward earnings multiple. Even with the substantial reduction to its adjusted earnings outlook, NCL is trading for 11 times the midpoint of this year's refreshed guidance and just 8 times next year's Wall Street profit target.

Looking out to 2027, Carnival stock is trading for 10 times projected earnings. Royal Caribbean's year-ahead multiple is 13. These are discounts to the overall market, but not NCL's single-digit multiple. Viking hit an all-time high after posting blowout results a week after NCL's disappointing update and understandably trades at a premium multiple to its peers, given its differentiated product and wealthy clientele that is better suited to absorb any pricing increases.

This brings us back to Chidsey. NCL's CEO is making a statement with last week's substantial purchase. The industry headwinds are clearly there. Fuel costs keep rising, and the geopolitical climate isn't kind to folks planning to hop on an ocean getaway for a few days, if not longer.

Buying NCL just because it's the cheapest cruise line stock isn't the right thesis to hitch your portfolio to these days. As I pointed out earlier this month, NCL was also the cheapest stock a year ago. We know how well that played out. However, the insider buying is interesting.

The near-term forecast is gloomy. When NCL hosed down its full-year outlook, it also cut its net yield forecast. This is a popular industry metric that scores net revenue per available passenger cruise day, with certain variable expenses backed out. It's now negative, another contrast to its better-performing peers.

However, let's see how the stock performs now that there is a key milestone of insider buying. As long as NCL stock isn't trading even lower the next time Chidsey is buying -- if there is a next time -- this could have been a clear signal that NCL is finally too cheap to ignore.

Rick Munarriz has positions in Royal Caribbean Cruises and Viking. The Motley Fool has positions in and recommends Viking. The Motley Fool recommends Carnival Corp. The Motley Fool has a disclosure policy.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English