Has The Recent Pullback In Waste Management (WM) Opened A Valuation Opportunity?

- Wondering whether Waste Management at around US$211.46 per share offers fair value or a possible opportunity? This article focuses squarely on what the current price could mean for you.

- The stock has pulled back recently, with returns declining 3.0% over the past week, 7.6% over the past month, and 3.2% year to date. The 1 year return is down 10.9%, set against a 3 year gain of 33.6% and a 5 year gain of 61.8%.

- Recent headlines have centered on Waste Management as a major US waste services provider, often highlighting its role as a core infrastructure style stock in many portfolios and the broader interest in essential service companies. This context helps explain why recent price moves may have attracted attention from investors who monitor defensive and cash flow focused businesses.

- On Simply Wall St, Waste Management currently has a valuation score of 3 out of 6, which points to some areas where the stock screens as undervalued and others where it does not. The rest of this article will unpack how different valuation methods arrive at that view and then look at an even more comprehensive way to think about value by the end.

Approach 1: Waste Management Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows, then discounts them back to today to estimate what the business could be worth in the present. It is essentially asking what a stream of future cash in your pocket is worth right now.

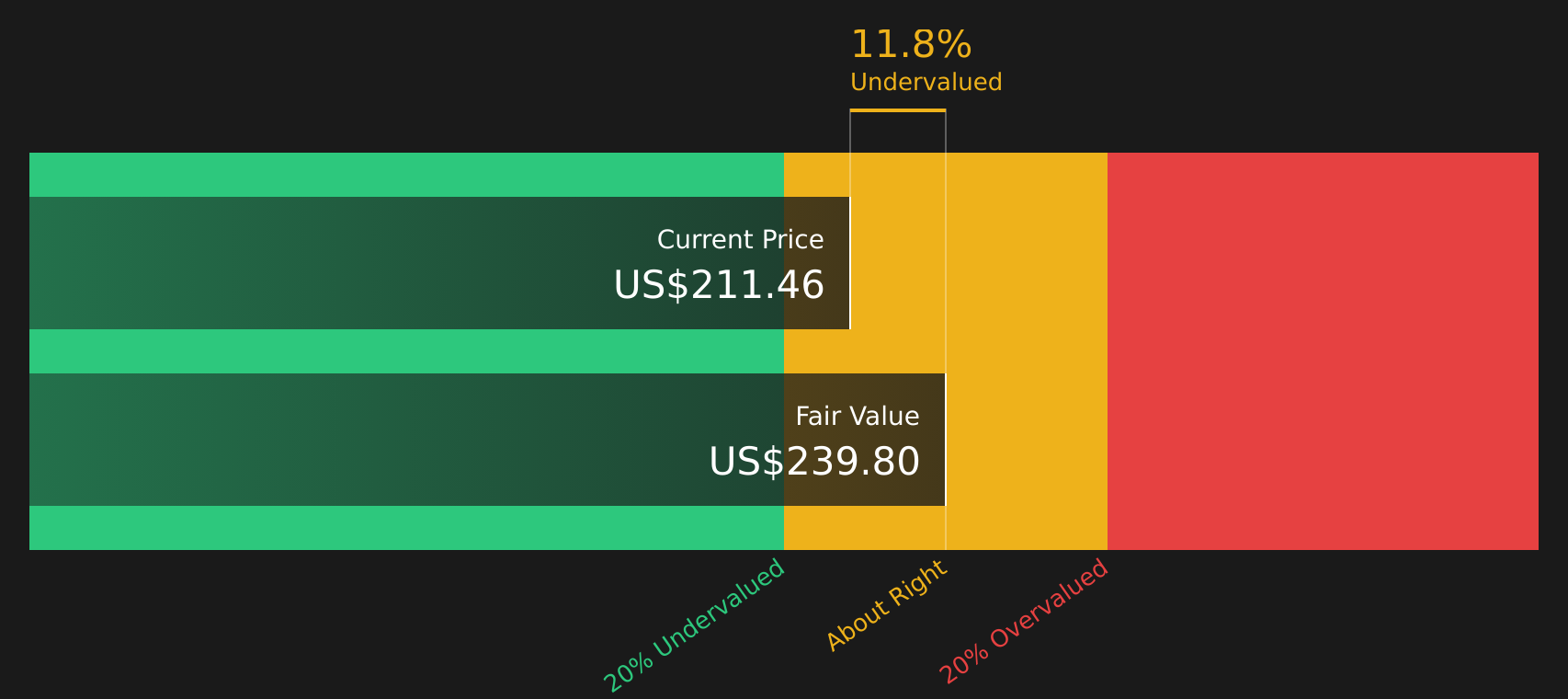

For Waste Management, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $2.9b. Analyst estimates and Simply Wall St extrapolations project Free Cash Flow reaching around $4.8b in 2035, with a path that includes $4.5b in 2030. All figures are in $ and already converted into today’s money using a discount rate.

When all those discounted cash flows are added up, the DCF model arrives at an estimated intrinsic value of about $239.80 per share. Against a current share price of around $211.46, this implies the stock trades at roughly an 11.8% discount, so the DCF view is that the stock looks slightly undervalued at today’s level.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Waste Management is undervalued by 11.8%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Waste Management Price vs Earnings

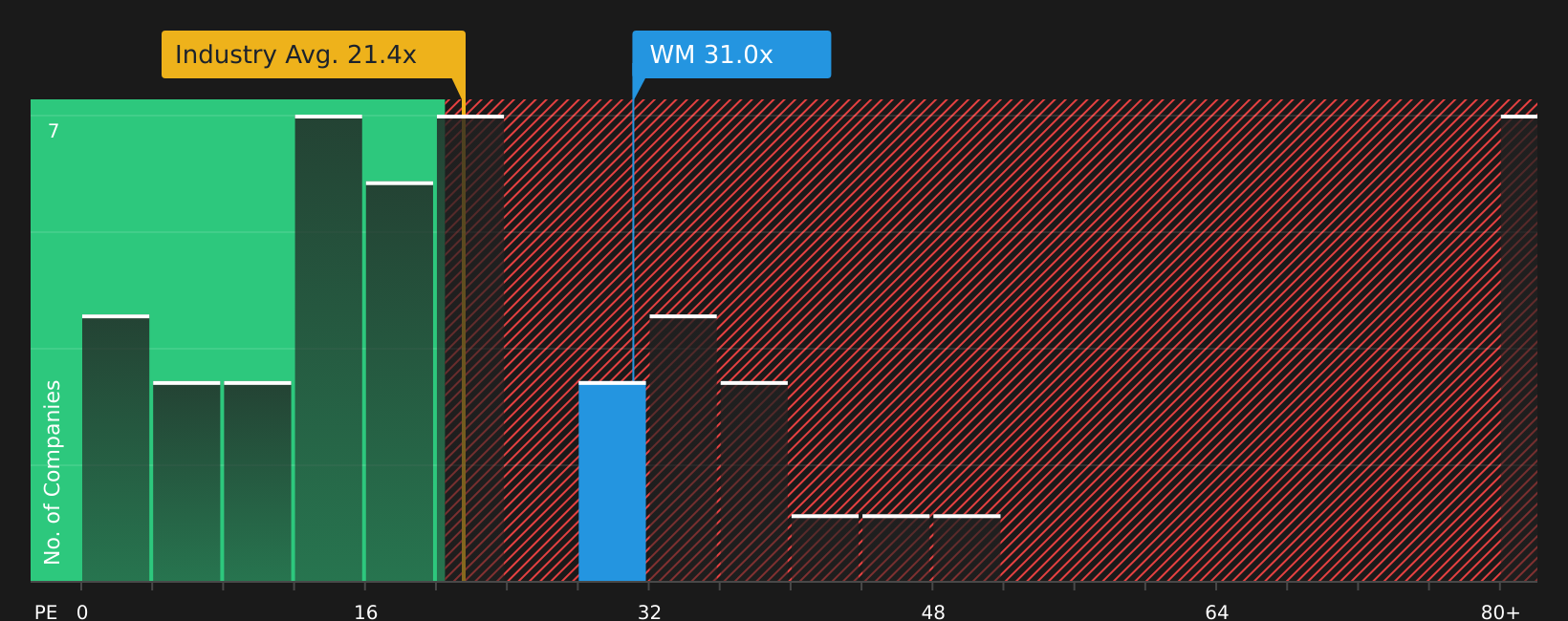

For profitable companies, the P/E ratio is a useful way to relate what you are paying for each share to the earnings that the business is currently generating. It gives you a quick sense of how many years of current earnings the market is pricing into the stock.

What counts as a “normal” or “fair” P/E depends on how the market views a company’s growth prospects and risk. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth expectations or higher risk typically point to a lower P/E.

Waste Management currently trades on a P/E of about 30.4x. This sits above the Commercial Services industry average of around 21.4x, but slightly below the peer group average of about 32.1x. Simply Wall St also provides a proprietary “Fair Ratio”, which estimates what P/E might be appropriate after considering factors such as earnings growth, profit margins, industry, market cap and risk. For Waste Management, this Fair Ratio is 29.8x.

Because the Fair Ratio is tailored to the company’s specific profile, it can be more informative than simple peer or industry comparisons. With the actual P/E of 30.4x sitting close to the Fair Ratio of 29.8x, the multiple view suggests the stock is trading near a reasonable level.

Result: ABOUT RIGHT

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Waste Management Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are a simple way for you to write the story behind your numbers by linking your view of Waste Management’s future revenue, earnings and margins to a financial forecast and then to a fair value. This is done through an easy tool on Simply Wall St’s Community page that updates automatically when new information like news or earnings arrives.

In practice, Narratives help you decide what action makes sense by comparing your own fair value to the current share price. For example, one investor might build a Narrative close to the higher analyst price target of US$277.00 if they focus on technology, sustainability projects and healthcare integration. Another might lean toward the lower target of US$198.00 if they place more weight on risks such as regulatory changes, leverage or revenue volatility. Both perspectives are visible side by side on the platform for you to compare with your own view.

Do you think there's more to the story for Waste Management? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English