A Look At DICK'S Sporting Goods (DKS) Valuation After Strong Q1 Results And Lower Full Year Guidance

Quarterly results and guidance reset

DICK'S Sporting Goods (DKS) reported first quarter revenue of US$5,164.5 million and net income of US$319.82 million, while at the same time trimming its full year net sales, operating income and earnings guidance.

The company now projects full year net sales of US$22.1 billion to US$22.4 billion, operating income of US$1,688 million to US$1,806 million, and earnings per diluted share of US$13.27 to US$14.27.

See our latest analysis for DICK'S Sporting Goods.

DICK'S Sporting Goods' first quarter report, guidance reset, recent AI powered Coach by DICK'S app launch and an updated share repurchase program all landed against a share price of US$227.57, with a 90 day share price return of 12.96% and a 1 year total shareholder return of 32.08%. This combination suggests that momentum has been building over both shorter and longer periods.

If this mix of earnings, guidance changes and new digital tools has you thinking about where else growth stories might develop, it could be worth scanning 20 top founder-led companies

With the stock up 32.08% over the past year and trading near analysts’ average price target, the key question is whether DICK'S Sporting Goods is still mispriced or if the market is already factoring in future growth.

Most Popular Narrative: 3% Undervalued

Compared with the last close at $227.57, the most followed narrative places DICK'S Sporting Goods' fair value at $234.76, implying a modest valuation gap built on detailed long term forecasts and a 9.33% discount rate.

The acquisition of Foot Locker is set to expand DICK'S total addressable market, broaden its consumer base, strengthen vendor relationships, and offer synergies (targeting $100 to $125 million), all of which are likely to accelerate top-line growth and operating earnings post-integration.

Curious what underpins that fair value? The narrative leans on multi year revenue expansion, rising profit margins and a richer earnings base shaped by the Foot Locker integration.

Result: Fair Value of $234.76 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on the Foot Locker turnaround and on higher footwear exposure not weighing on margins or growth if consumer demand or store traffic softens.

Find out about the key risks to this DICK'S Sporting Goods narrative.

Another View: Market Multiple Sends A Different Signal

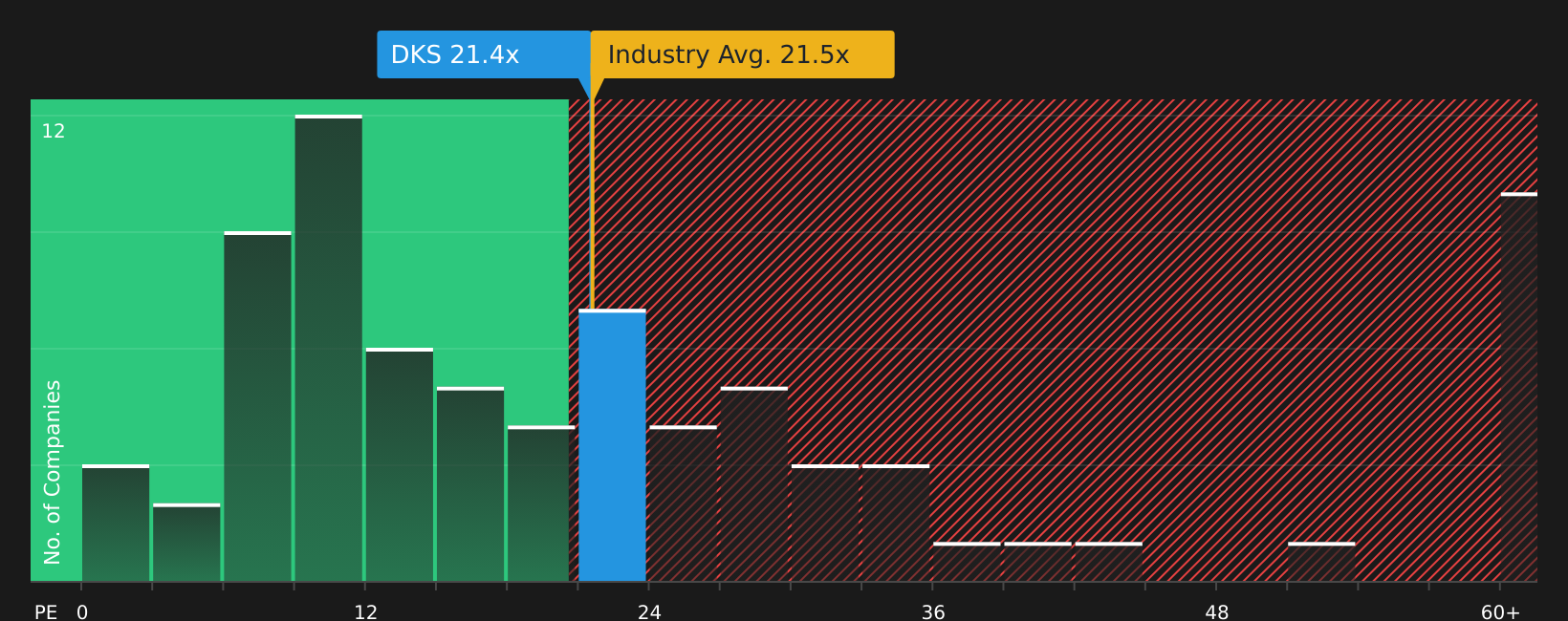

While the narrative suggests a small undervaluation, the current P/E of 22.5x is higher than both the US Specialty Retail industry at 21.9x and the fair ratio of 20.4x. This points to a richer pricing that could limit upside if expectations slip even slightly.

That mix of a premium P/E versus industry and fair ratio leaves you weighing whether the stock is pricing in too much good news already or whether the peer gap reflects something more durable in the business. That is where a closer look at the underlying drivers can really matter. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given this mix of potential risks and rewards, it makes sense to move quickly, review the full picture, and decide where you stand using 1 key reward and 3 important warning signs

Looking for more investment ideas?

If DICK'S Sporting Goods has sharpened your focus on valuation and quality, do not stop here, broaden your watchlist with other well screened opportunities.

- Target quality today by scanning 46 high quality undervalued stocks that pair solid fundamentals with prices that still sit below their estimated worth.

- Strengthen your income stream by reviewing 10 dividend fortresses that combine yields above 5% with an emphasis on durability.

- Prioritize resilience by checking 64 resilient stocks with low risk scores designed to highlight companies with lower risk scores and steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English