A Look At Starwood Property Trust (STWD) Valuation After Recent Share Price Weakness

Recent share performance and income profile

Starwood Property Trust (STWD) has drawn fresh investor attention after a recent move in its share price, with the stock closing at US$17.10 and showing mixed returns over different time frames.

Over the past month the stock is down 6.6%, and over the past 3 months it is down 5.5%. Year to date, the total return is down 7.2%, while the 1 year total return is down 4.5%.

Longer term holders see a different picture, with total return over 3 years at 24.2% and over 5 years at 3.0%. These figures give you a sense of how the recent pullback fits within its multi year record.

Starwood Property Trust operates as a real estate investment trust (REIT), with four segments that span commercial and residential lending, infrastructure lending, property ownership, and an investing and servicing business focused on managing and working out problem assets.

On the income side, the company reports annual revenue of US$580.8m and net income of US$341.7m, with reported annual revenue growth of 39.3% and net income growth of 20.4%. For investors focusing on stability and income, the REIT structure and earnings profile are often central to the investment case.

See our latest analysis for Starwood Property Trust.

Putting this in context, the recent 1 day share price gain of 1.8% to US$17.10 comes after the share price declined 7.2% year to date. The 3 year total shareholder return of 24.2% indicates earlier gains are being digested and recent momentum has faded.

If you are comparing STWD with other income or real asset ideas, it can help to widen the lens and see what else is moving, including opportunities highlighted in our 33 power grid technology and infrastructure stocks

With STWD trading at US$17.10 and sitting at a discount to some valuation estimates, the key question for you is simple: Is this recent weakness an opening to buy in, or is the market already pricing in future growth?

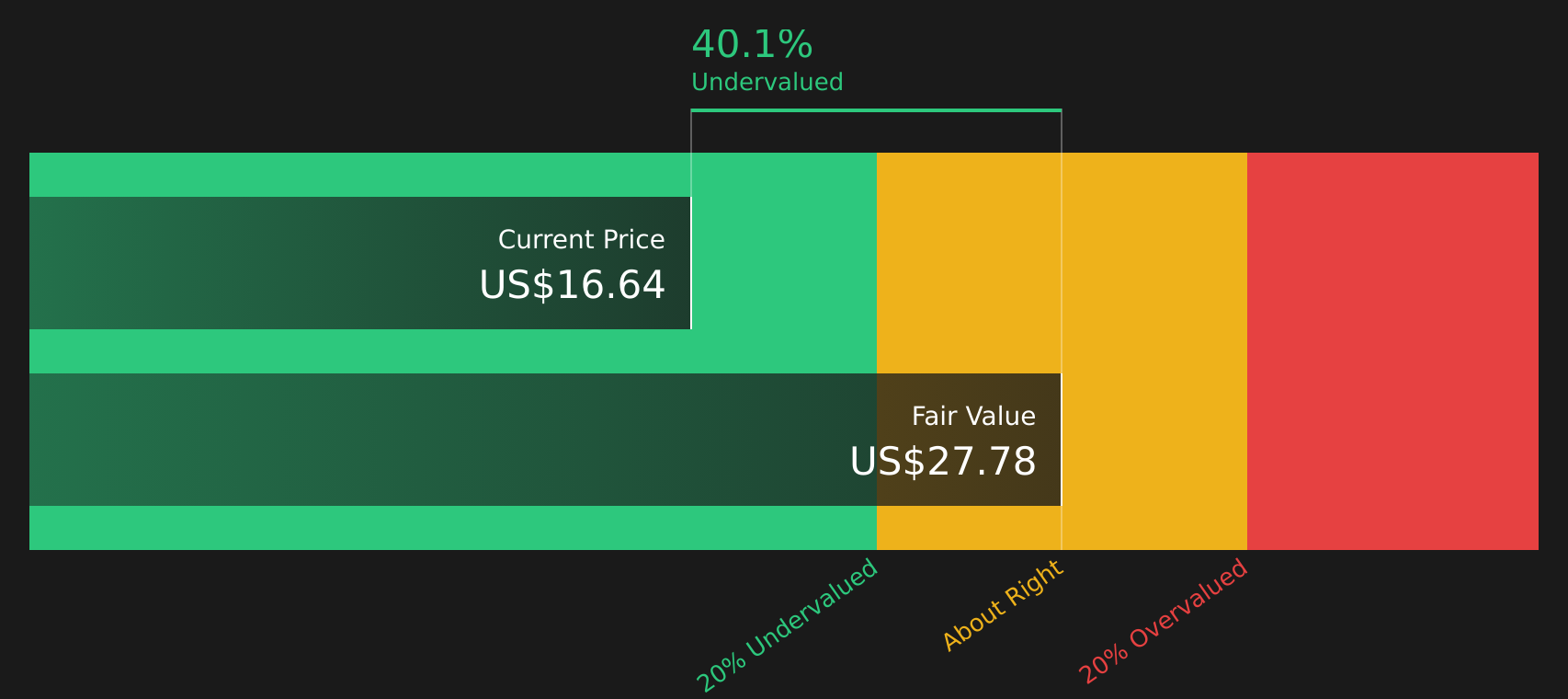

Most Popular Narrative: 16% Undervalued

At $17.10, the most followed narrative implies a fair value of about $20.36, which puts Starwood Property Trust at a clear discount in that framework while still baking in a meaningful risk adjustment.

Analysts are assuming Starwood Property Trust's revenue will grow by 78.7% annually over the next 3 years. Analysts expect earnings to reach $626.4 million (and earnings per share of $1.43) by about May 2029, up from $341.7 million today. Read the complete narrative.

It is worth asking what kind of revenue change and margin reset would need to align for that fair value to hold. The projected earnings change, the lower profit share, and the future P/E all have to work together. The full narrative lays out how those moving parts stack up across several years, not just the next quarter.

Result: Fair Value of $20.36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the bullish narrative could be challenged if credit issues around nonaccrual assets deepen, or if integration of the Fundamental Income acquisition drags on earnings and margins.

Find out about the key risks to this Starwood Property Trust narrative.

Another View: Earnings Power Versus Market Multiple

There is a sharp contrast between the SWS DCF model and how the market is currently pricing Starwood Property Trust. On one side, the stock trades at a P/E of 18.6x, higher than both the US Mortgage REITs industry at 11.7x and the peer average at 15.3x, as well as above its fair ratio of 14.8x.

On the other side, the SWS DCF model estimates a future cash flow value of US$27.05, which is higher than both the current share price of US$17.10 and the analyst fair value of about US$20.36. That mix of a richer earnings multiple but a large DCF gap raises a simple question for you: is the market overpaying for current earnings or underestimating future cash flows?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Mixed messages in the data, or a balanced risk and reward setup that needs a closer look? Act while the information is fresh and weigh the trade offs for yourself with our 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might suit your goals, income needs, or risk comfort better.

- Spot potential bargains by scanning the market for quality companies trading at discounts using the 46 high quality undervalued stocks.

- Strengthen your income stream by focusing on businesses that combine higher yields with resilient payouts through the 11 dividend fortresses.

- Reduce surprises in your portfolio by concentrating on companies that score well on stability and financial resilience with the 63 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English