A $2 Billion Reason to Buy Little-Known Gorilla Technology Stock Right Now

While the rally in technology stocks continues, there are some near-term valuation concerns. There might not be a technology bubble, but some correction from highs seems desirable. However, under-the-radar opportunities still exist with attractive valuations. One name that deserves mention and consideration for the portfolio is Gorilla Technology (GRRR) .

Gorilla is a global AI infrastructure solutions provider, and GRRR stock has returned 64% year-to-date (YTD). With some big order intakes in the last few quarters, Gorilla seems to be positioned for significant value creation.

Recently, Gorilla signed a $2 billion AI infrastructure deal with Super Micro Computer (SMCI) in India. Under this deal, Super Micro will deliver 20,736 B300 cards, 5,120 B200 cards, networking equipment, and related infrastructure to support Gorilla's Yotta project.

Further, Supermicro and Gorilla will collaborate to pursue AI infrastructure opportunities across India and Asia Pacific. The contract underscores the growth potential for Gorilla. As the backlog translates into order execution and growth, GRRR stock is likely to be re-rated.

About Gorilla Stock

Incorporated in 2001 and headquartered in London, Gorilla Technology is a solution provider specializing in security intelligence, network intelligence, business intelligence, and the Internet of Things (IoT).

With a strong global presence, Gorilla is focused on delivering AI-driven solutions for smart cities, enterprises, government, manufacturing, retail, ports, and more. With innovation as the backbone, Gorilla has 28 approved and three pending patents.

The company is still in an early-growth stage, and for FY25, revenue increased by 36% on a year-on-year (YoY) basis to $101.4 million. However, as the company’s contract backlog swells, there is a strong case for significant growth acceleration.

From that perspective, GRRR stock looks attractive even after a rally of 29% in the past six months. That said, a fresh bond offering announced this morning is weighing heavily on the stock. GRRR is down over 18% in early morning trading as investors factor in dilution concerns.

Flurry of Order Wins

A key reason to be bullish on Gorilla is the company’s swelling order backlog. In September 2025, the company announced a $1.4 billion contract with Freyr for data centers and GPUaaS across Southeast Asia. Further, in January 2026, Gorilla won a multi-year contract with a law enforcement agency and criminal investigation bureau in the Asia-Pacific region.

In another major win in March 2026, the company announced a $500 million contract with Yotta Data Services over a period of five years. However, in April 2026, this contract was expanded to $2.8 billion. Overall, these contracts are likely to translate into meaningful growth acceleration.

It’s also worth noting that the company expects 52% of FY26 revenue from Asia and 28% from Europe, the Middle East, and Africa (EMEA). There is ample scope for making inroads in the U.S. and LATAM (20% of total revenue).

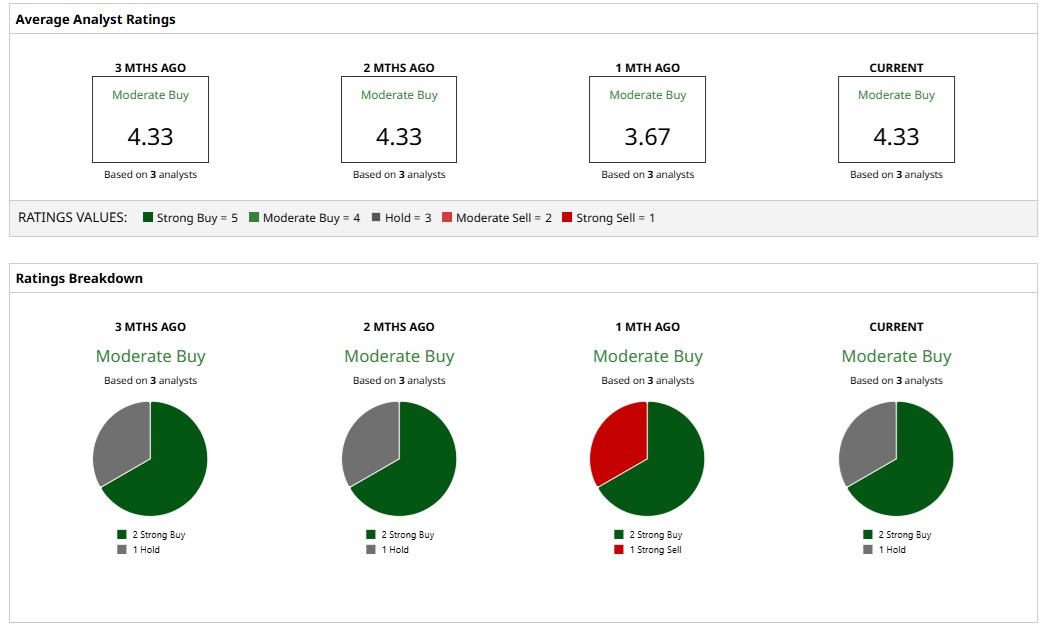

What Do Analysts Say About GRRR Stock?

Based on three analysts with coverage, GRRR stock has a consensus “Moderate Buy” rating. While two analysts have a “Strong Buy” rating for GRRR stock, one analyst has a “Hold” rating.

The mean price target of $36.67 represents a potential upside of 105% from current levels. Further, the most bullish price target of $40 suggests that GRRR could climb 125% from here.

Concluding Views

From a valuation perspective, GRRR stock trades at a forward price-earnings ratio of 12.72. This seems attractive considering the point that for FY26 and FY27, analysts expect earnings growth of 82.95% and 60.87%, respectively.

Last year was transformational for the company with multiple orders and an equity raise of $105 million. The next 12 to 24 months are likely to be focused on execution that will boost revenue and cash flows.

To put things into perspective, Jay Chandan, the company’s chairman and CEO, believes that the Yotta agreement presents an annual revenue opportunity of $500 million. If the execution is right, FY27 revenue is likely to be around $500 million. Q1 FY26 already provides an indication with revenue growth of 55% coupled with a healthy full-year guidance of $180 million (mid-range). With these factors in consideration, GRRR stock looks attractive.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English