How CNH’s Case IH–New Holland “Purpling” Strategy Will Impact CNH Industrial (CNH) Investors

- Earlier this week, CNH Industrial reorganized its North America commercial business by combining management of its Case IH and New Holland dealer networks, a “purpling” move intended to streamline support while keeping the brands distinct.

- This consolidation has drawn mixed reactions from dealers but highlights CNH’s push for cost efficiency and closer coordination across its agricultural equipment channels.

- We’ll now examine how this “purpling” of Case IH and New Holland could reshape CNH Industrial’s investment narrative and operational priorities.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

CNH Industrial Investment Narrative Recap

To own CNH Industrial today, you generally need to believe that its ag and construction equipment franchises can convert technology investments and cost discipline into better margins over time, despite current operational pressures and debt. The “purpling” of Case IH and New Holland looks more like an execution and cost-efficiency experiment than a fundamental shift to the near term story, where the key catalyst is margin improvement and the biggest risk is ongoing weakness in North American agriculture.

The recent dividend cut to US$0.10 per share for 2025 is the announcement that most sharpens this context. It underlines how thin current profitability is, with Q1 2026 net income at just US$7 million, and shows management prioritizing balance sheet resilience while it works on initiatives like dealer consolidation and tech-enabled services that many investors see as crucial to any future margin recovery.

Yet behind the “purpling” story, investors should be aware that rising inventories and channel destocking in North America could still...

Read the full narrative on CNH Industrial (it's free!)

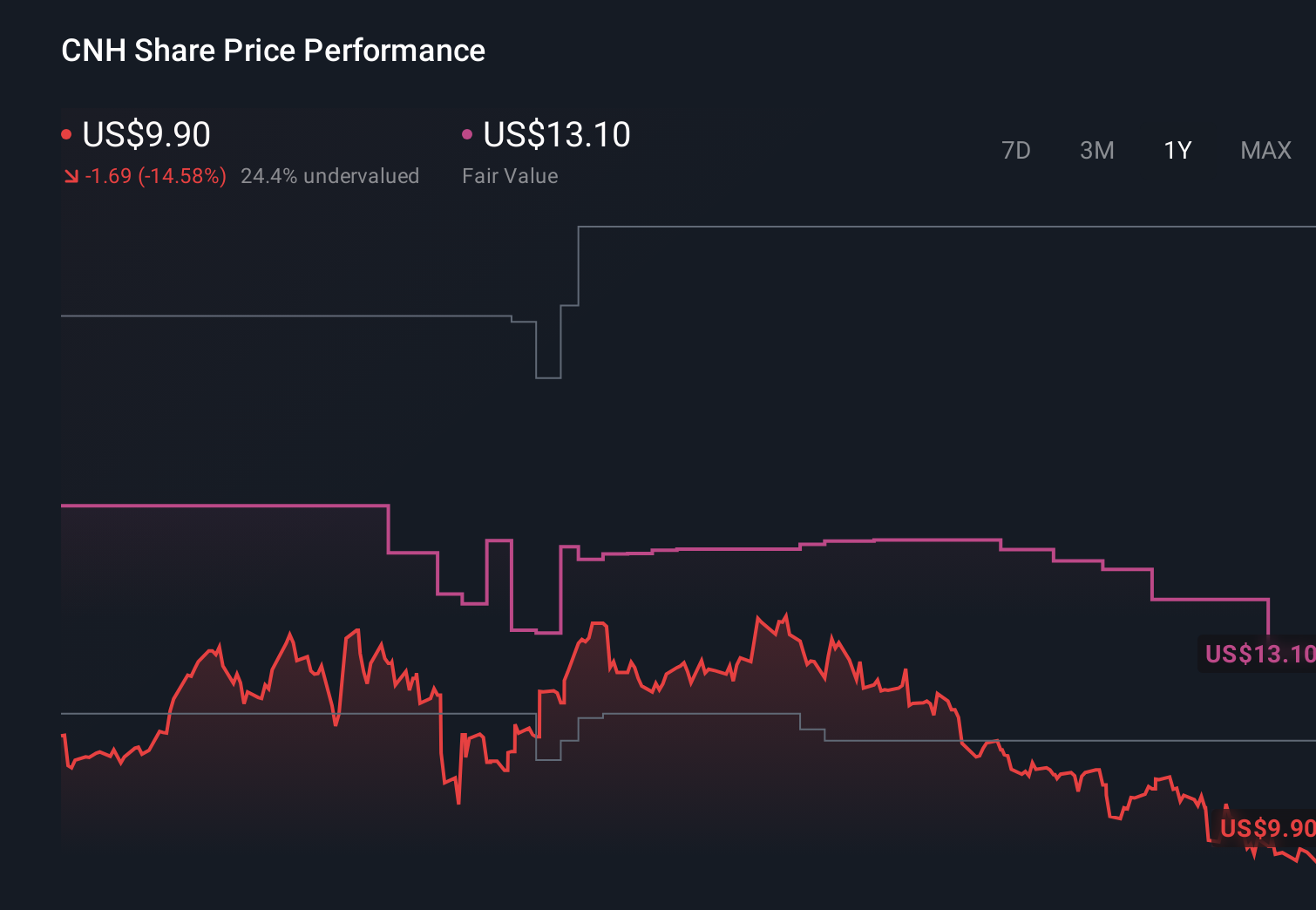

CNH Industrial's narrative projects $20.9 billion revenue and $1.4 billion earnings by 2029. This requires 4.8% yearly revenue growth and about a $1.0 billion earnings increase from $386.0 million today.

Uncover how CNH Industrial's forecasts yield a $13.36 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenues around US$18.4 billion and earnings near US$1.1 billion by 2028, and they see tariff driven cost pressures as a direct threat, offering a much more pessimistic counterpoint to the more optimistic tech and efficiency focused thesis that the new Case IH and New Holland structure now puts back in the spotlight.

Explore 5 other fair value estimates on CNH Industrial - why the stock might be worth as much as 71% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CNH Industrial research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free CNH Industrial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNH Industrial's overall financial health at a glance.

No Opportunity In CNH Industrial?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English