A Look At American Healthcare REIT (AHR) Valuation After Analyst Upgrades On Strong Q1 And Raised Guidance

American Healthcare REIT (AHR) is back in focus after robust Q1 results, higher than expected FFO and raised full year guidance prompted several analysts to upgrade their outlook on the stock.

See our latest analysis for American Healthcare REIT.

Despite the upbeat Q1 and upcoming Nareit REITweek appearance, the stock’s recent performance has been mixed. The share price is down 7.82% over 90 days and 5.08% over 30 days, while the 1-year total shareholder return of 37.01% points to momentum that has built over a longer horizon.

If you are looking for more ideas in healthcare-related real estate and services, it can be useful to compare AHR with other opportunities using our screener for 39 healthcare AI stocks

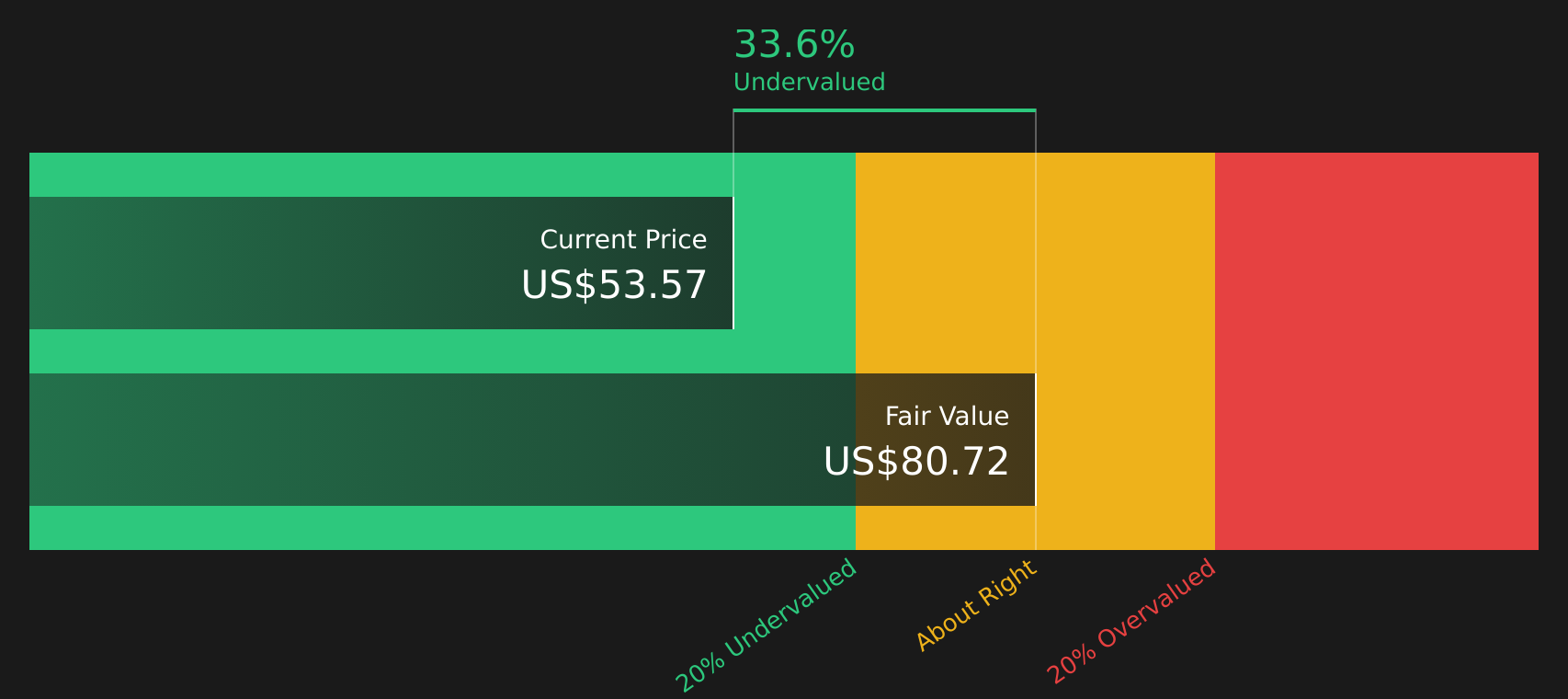

With American Healthcare REIT trading at $47.48, carrying an indicated intrinsic discount of 37.37% and a 23.94% gap to the average analyst price target of $58.85, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 19.3% Undervalued

At $47.48, American Healthcare REIT trades below a narrative fair value of $58.85, setting up a sizeable gap between price and expectations.

The company's disciplined portfolio optimization selling older, lower-quality assets and redeploying proceeds into modern, higher-acuity, and recently developed properties at below replacement cost should improve asset quality and accelerate future AFFO and earnings growth as new assets stabilize. Scalable operating initiatives, such as advanced revenue management systems and best-in-class benchmarking across operators, are expected to further increase pricing power and operational efficiency, translating into continued net margin improvement and higher cash flows.

Curious what kind of revenue path and margin uplift supports a fair value above $58 per share? The narrative leans on ambitious growth, a richer mix, and a premium earnings multiple that is closer to high growth sectors than typical REITs.

Result: Fair Value of $58.85 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change quickly if occupancy momentum flattens, or if reimbursement pressure from Medicaid and Medicare Advantage starts to squeeze margins more than expected.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle on Valuation

The SWS DCF model points to a fair value of $75.81 per share, which sits well above both the current $47.48 price and the $58.85 narrative fair value. That gap suggests even more upside in the cash flow view. It also raises a question: which set of assumptions do you trust most?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Seen enough optimism and caution to know this story is finely balanced? Act while sentiment is still split and review the 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop your research here, you could miss stocks that better match your goals, risk comfort, and income needs, so keep widening your opportunity set.

- Hunt for potential mispricings by scanning companies that look cheap on quality metrics using our 49 high quality undervalued stocks.

- Target reliable income by reviewing stocks with robust yields and payout profiles through the 9 dividend fortresses.

- Prioritize resilience by focusing on companies with stronger finances and cleaner balance sheets in the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English