Why Axon Enterprise (AXON) Is Up 8.3% After Expanding Its Drone Ecosystem With Echodyne

- In late May 2026, Echodyne announced a partnership with Axon Enterprise to integrate its MESA radar into Axon’s public safety drone ecosystem, enhancing low-altitude airspace awareness for both authorized and unauthorized drone activity worldwide.

- At the same time, Motorola Solutions’ US$1.5 billion acquisition of counter-drone specialist D-Fend Solutions intensifies head-to-head competition with Axon in drones, AI-enabled public safety technologies, and integrated hardware-software platforms.

- Against this backdrop, we’ll explore how Axon’s expanded drone ecosystem with Echodyne shapes its investment narrative amid rising Motorola competition.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Axon Enterprise Investment Narrative Recap

To own Axon, you need to believe public safety agencies will keep modernizing around its connected hardware, AI and cloud platform, despite valuation and competitive pressures. Right now, the key near term catalyst is execution on Axon’s real time intelligence and AI suite, while the biggest risk is intensifying competition, especially from Motorola. The Echodyne partnership strengthens Axon’s drone story, but does not materially change that near term risk reward balance.

Among recent announcements, the April launch of Axon Vision, Axon Assistant and Axon 911 is most relevant here. These real time intelligence tools sit on top of Axon’s installed hardware base and are central to the thesis that higher margin software and services can compound over time, even as Motorola bolsters its own capabilities with D Fend and pushes harder against Axon in drones, command centers and AI enabled workflows.

Yet investors should also weigh how rising regulatory and public scrutiny of AI driven surveillance tools could affect Axon’s long term growth potential and margins...

Read the full narrative on Axon Enterprise (it's free!)

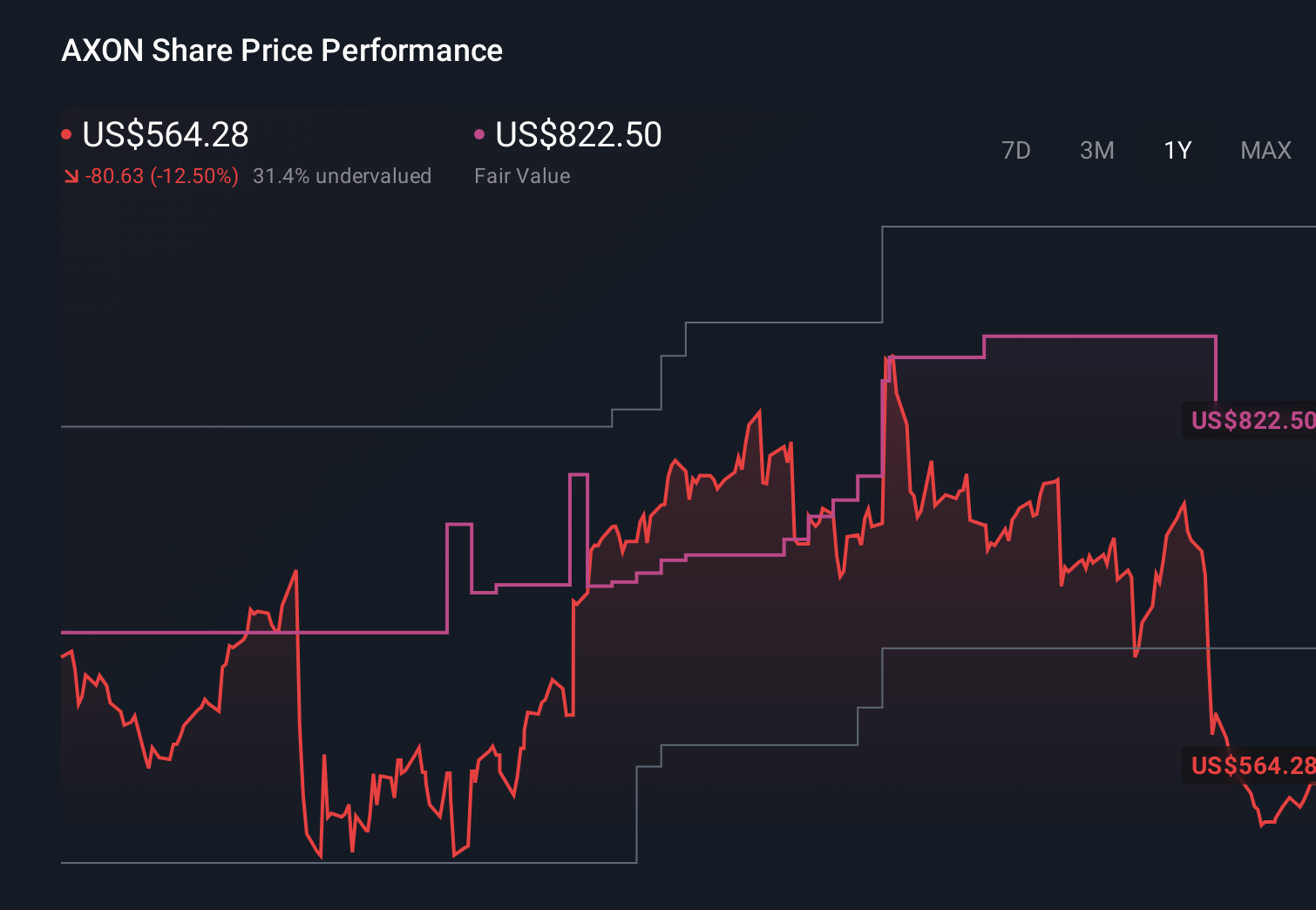

Axon Enterprise's narrative projects $6.3 billion revenue and $516.8 million earnings by 2029.

Uncover how Axon Enterprise's forecasts yield a $662.04 fair value, a 36% upside to its current price.

Exploring Other Perspectives

The most bullish analysts were already assuming about US$4.5 billion revenue and US$641.9 million earnings by 2028, so this Echodyne news could either reinforce or challenge those expectations, depending on how you view Axon’s competitive and regulatory risks.

Explore 9 other fair value estimates on Axon Enterprise - why the stock might be worth 21% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Axon Enterprise research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Axon Enterprise research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Axon Enterprise's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English