Is Aeva Technologies’ (AEVA) New Capital Raise Quietly Redefining Its Intelligent Infrastructure Ambitions?

- Aeva Technologies recently closed a follow-on public offering of common stock that raised about US$115.0 million and is showcasing its AI-powered CityOS traffic intelligence platform, built on its 4D LiDAR and edge AI technology, to transportation agencies at the ITS America 2026 Conference & Expo.

- These moves highlight how Aeva is pairing fresh capital with expanding real-world deployments in intelligent infrastructure and sensing partnerships to support commercialization of its FMCW technology across automotive, industrial, and smart-city markets.

- We’ll now examine how Aeva’s US$115.0 million capital raise and push into AI-powered traffic infrastructure may influence its existing investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Aeva Technologies Investment Narrative Recap

To own Aeva, you need to believe its FMCW LiDAR and perception software can turn early design wins in auto, trucking, and industrial sensing into durable, scaled programs. In the near term, the key catalyst is progress toward a series production award with a top 10 passenger OEM, while the biggest risk is that long design cycles or program changes delay that decision. The US$115.0 million raise and CityOS push support commercialization but do not remove that execution risk.

Among the recent announcements, the expansion of Aeva’s FMCW collaboration with SICK stands out alongside CityOS. SICK’s adoption of Aeva technology for demanding industrial measurement ties directly into the diversification catalyst away from purely automotive revenue and into manufacturing automation. Taken together with new AI traffic deployments, this suggests that industrial and infrastructure sensing are becoming more meaningful testbeds for Aeva’s core FMCW platform while investors wait on larger auto and trucking ramps.

Yet behind the fresh capital and new deployments, investors should still be aware of the risk that extended OEM timelines and concentrated programs could...

Read the full narrative on Aeva Technologies (it's free!)

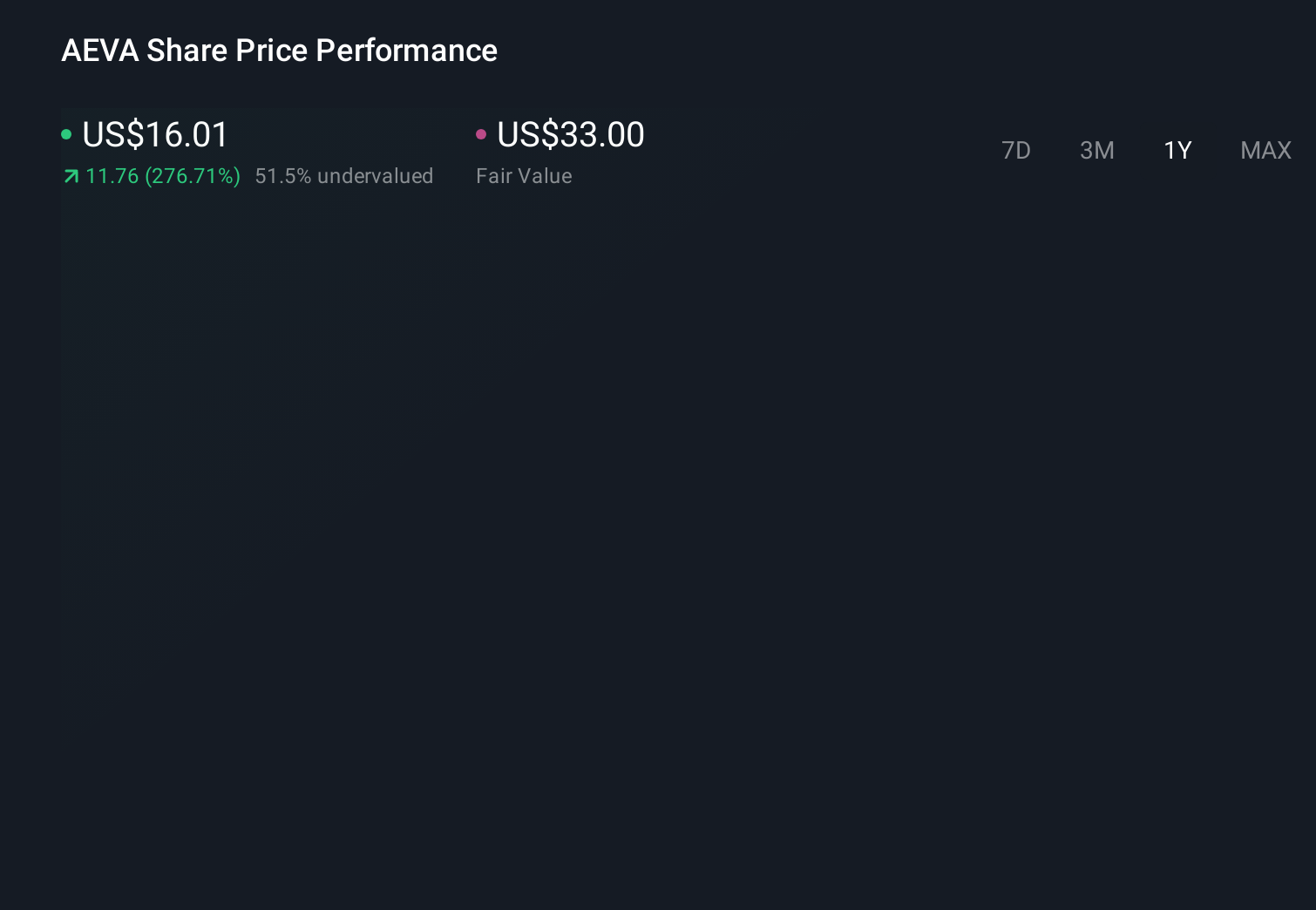

Aeva Technologies' narrative projects $192.0 million revenue and $16.8 million earnings by 2028. This requires 133.1% yearly revenue growth and about a $173 million earnings increase from -$156.3 million today.

Uncover how Aeva Technologies' forecasts yield a $24.11 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming Aeva might need US$201.0 million of revenue and only US$17.0 million of earnings by 2029, so if you see CityOS and SICK adoption as evidence that programs could remain slow and concentrated rather than broad based, your view may align more with this more pessimistic camp.

Explore 5 other fair value estimates on Aeva Technologies - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Aeva Technologies research is our analysis highlighting 2 key rewards and 5 important warning signs that could impact your investment decision.

- Our free Aeva Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Aeva Technologies' overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English