Applied Digital (APLD) Stock Jumps on Data Center Deal

Applied Digital (APLD) shares were in favor on June 9 after the company announced its third 15-year lease agreement with an undisclosed U.S.-based investment-grade hyperscaler.

The new deal involves 210 megawatts of critical IT load at Delta Forge 2, the firm’s fifth artificial intelligence (AI) factory campus, located in an undisclosed southern state.

The take-or-pay lease structure guarantees about $5.2 billion in base-term contracted revenue, with potential to reach $12.7 billion if all renewal options are exercised over a 30-year total term.

Applied Digital stock is currently up more than 100% versus its year-to-date low in late March.

Why the Announcement Is Bullish for Applied Digital Stock

The said agreement follows a remarkable deal-signing cadence, coming just 18 days after APLD’s Polaris Forge 3 announcement and roughly six weeks after the Delta Forge 1 lease was signed.

The cumulative effect of these contracts has pushed Applied Digital’s overall contracted base-term lease revenue to $36 billion across five campuses, or $86 billion including all renewal options.

A remarkable 70% of the firm’s contracted revenue is now backed by U.S.-based investment-grade hyperscalers.

APLD Announces Private Debt Offering

On Tuesday, Applied Digital also announced a $1.59 billion offering of senior secured notes due 2031 through its subsidiary APLD ComputeCo 3.

Proceeds are earmarked for a 150 megawatts boost at the fourth building of Polaris Forge 1 in North Dakota and repayment of a Goldman Sachs bridge loan.

The private debt offering follows the closure of a $350 million revolving credit facility with a $200 million accordion option, showcasing management’s aggressive approach to securing construction financing.

APLD has also signed a memorandum of understanding with CoreWeave Inc to assign the Polaris Forge 1 Building 3 lease to its subsidiary, contingent upon that entity securing an investment-grade credit rating.

Some Caution Is Warranted in Playing APLD shares

Despite the positive momentum on contracted revenue, significant execution risks remain.

Applied Digital’s net loss stood at $101 million in fiscal Q3 and the company ended February with $2.7 billion in debt against $2.1 billion in cash and restricted cash.

APLD operates at a negative return on equity of about 16% and carries a “debt-to-equity ratio” of 1.65x, while initial operations at Delta Forge 2 are not expected until Q1 2028.

That said, the stock’s meteoric run reflects market confidence in the firm’s ability to convert scarce power assets and data center sites into long-dated contracted AI infrastructure capacity at a time when industry-wide demand continues to outstrip supply.

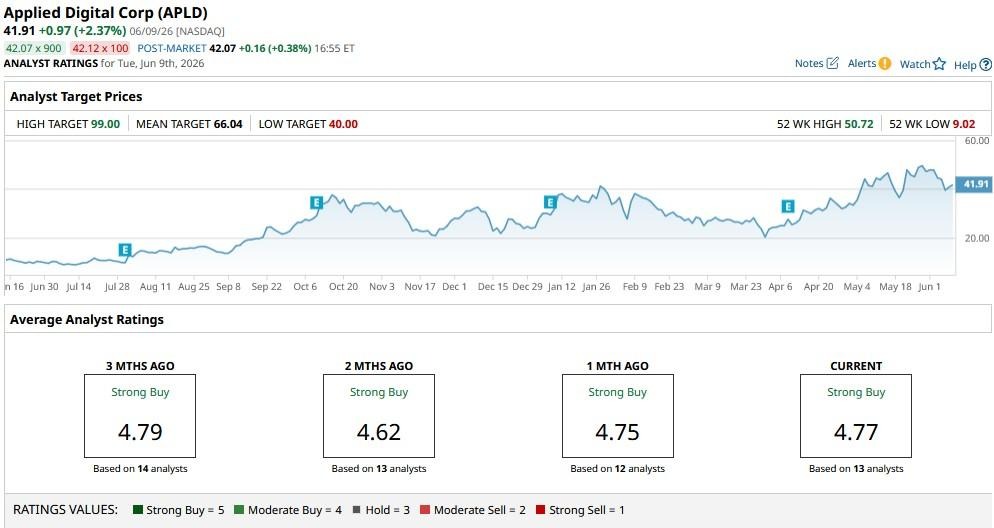

How Wall Street Recommends Playing Applied Digital

Wall Street responded to APLD’s new lease announcement with broad enthusiasm.

Lake Street raised its price objective to $90, Needham increased it to $83, Craig-Hallum moved to $79, and Compass Point lifted it to $70 on Tuesday morning.

The consensus rating on Applied Digital shares sits at “Strong Buy” currently with the mean price target of $66 indicating potential upside of nearly 60% from here.

Disclaimer: This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English