Is Tariff Relief Recasting CNH (CNH) as a Higher-Quality Agricultural Tech Platform?

- In recent days, CNH Industrial has drawn attention as the White House’s section 232 tariff reduction on agricultural equipment coincided with refreshed analyst assessments of the company’s fair value and earnings outlook.

- This combination of tariff relief and evolving views on CNH Industrial’s technology integration and execution risks has become a key focus for investors reassessing the company’s long-term prospects.

- Against this backdrop of tariff relief as a potential earnings tailwind, we’ll examine how the latest news reshapes CNH Industrial’s investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

CNH Industrial Investment Narrative Recap

To own CNH Industrial, you need to believe that its precision technology push and end market exposure can eventually translate into healthier margins, despite recent earnings pressure and mixed execution. The section 232 tariff reduction on agricultural equipment may offer a short term earnings boost, but it does not fundamentally alter the near term focus on margin recovery or the key risk around integrating new technology profitably.

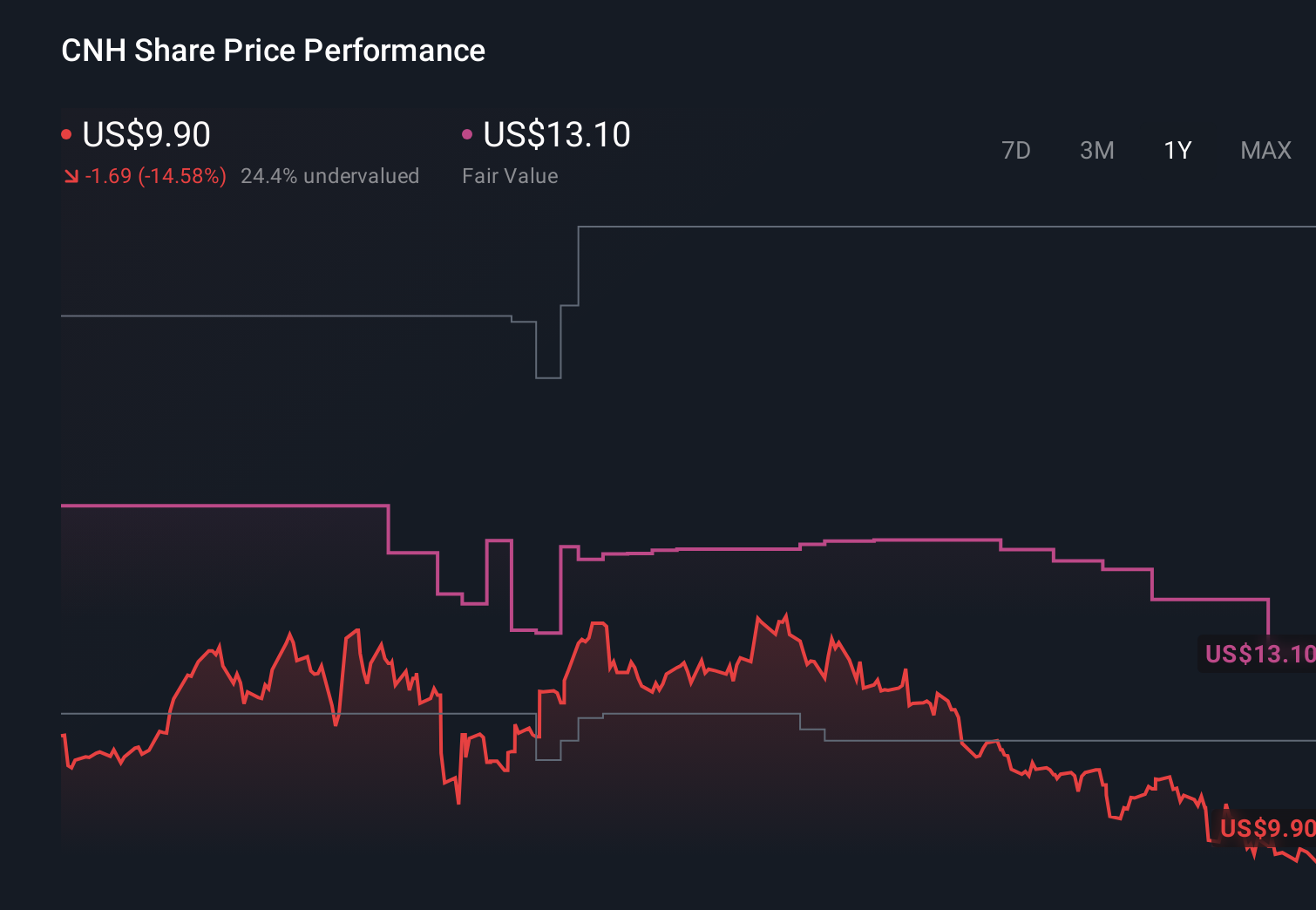

Among recent announcements, the sharp drop in Q1 2026 net income to US$7 million, from US$131 million a year earlier, feels most relevant. It highlights how fragile profitability currently is, even as some analysts see tariff relief as an earnings tailwind and argue the stock still trades below their fair value estimates, keeping the tension between valuation, execution risk, and earnings volatility front of mind.

Yet alongside tariff relief, investors should be aware that rising inventories and potential discounting pressure could still...

Read the full narrative on CNH Industrial (it's free!)

CNH Industrial's narrative projects $20.9 billion revenue and $1.4 billion earnings by 2029. This requires 4.8% yearly revenue growth and an earnings increase of about $1.0 billion from $386.0 million today.

Uncover how CNH Industrial's forecasts yield a $13.31 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue growth to about US$23.3 billion and earnings of US$2.3 billion by 2029, which is a far more upbeat story than consensus and could shift again as tariff changes and trade tensions evolve.

Explore 5 other fair value estimates on CNH Industrial - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CNH Industrial research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free CNH Industrial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNH Industrial's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English