WuXi Biologics (SEHK:2269) Stock After Regulatory Jitters And A 76.5% Five Year Slide

- If you are trying to figure out whether WuXi Biologics (Cayman) is attractively priced or not, a useful starting point is to separate short term share price noise from the company’s underlying value.

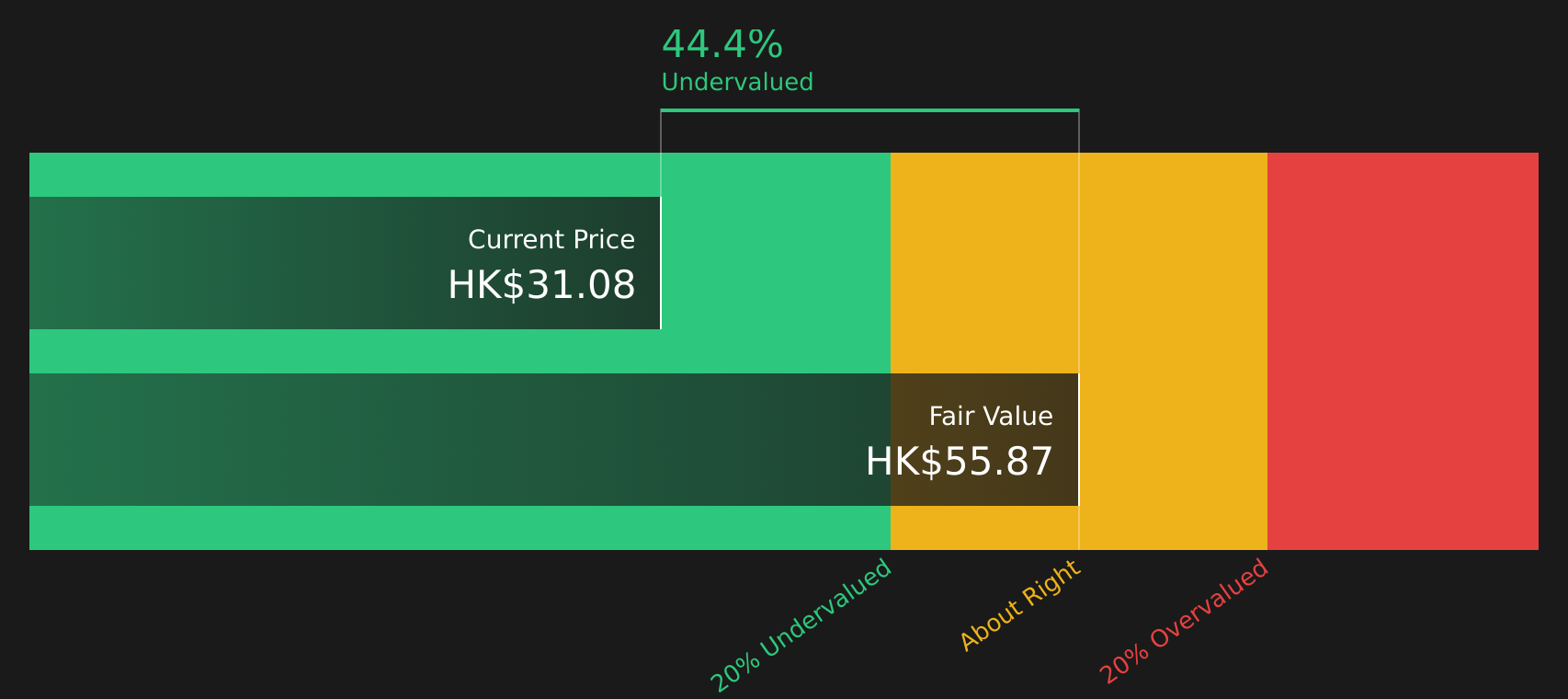

- The stock last closed at HK$31.08. The share price is up 11.0% over the past year but down 5.1% over the past week, 8.2% over the past month and 34.5% over three years, while the five year return is down 76.5%.

- Recent headlines around WuXi Biologics (Cayman) have focused on broader sector sentiment and regulatory attention, which can quickly change how investors price in future prospects. These shifts in mood help explain why the share price has moved very differently over shorter and longer time frames.

- On Simply Wall St's valuation checks, WuXi Biologics (Cayman) scores 4 out of 6, as shown in its valuation score. The rest of this article will walk through the main valuation approaches used, before finishing with a broader way to think about what the current price implies.

Approach 1: WuXi Biologics (Cayman) Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a stock could be worth by projecting future cash flows and discounting them back to today’s value. It focuses on the cash the business is expected to generate for shareholders over time.

For WuXi Biologics (Cayman), the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is CN¥1,895.34m. Analysts provide explicit forecasts out to 2028, with Simply Wall St extrapolating further to build a 10 year view. For example, projected Free Cash Flow reaches CN¥5,862.33m in 2028, with later years extending into the CN¥9b to CN¥14b range before discounting.

After discounting all these projected cash flows, the estimated intrinsic value is HK$55.77 per share. Compared with the recent share price of HK$31.08, this implies the stock is about 44.3% below the DCF estimate, which indicates that WuXi Biologics (Cayman) may be trading at a sizeable discount on this model.

Result: UNDERVALUED ON THIS DCF MODEL

Our Discounted Cash Flow (DCF) analysis suggests WuXi Biologics (Cayman) is undervalued by 44.3%. Track this in your watchlist or portfolio, or discover 193 more high quality undervalued stocks.

Approach 2: WuXi Biologics (Cayman) Price vs Earnings

For profitable companies, the P/E ratio is a practical way to think about valuation because it ties the share price directly to the earnings that each share represents. It helps you see how many years of current earnings the market is effectively paying for the stock.

What counts as a "normal" P/E will usually reflect how quickly earnings are expected to grow and how risky those earnings appear. Higher expected growth and lower perceived risk can justify a higher multiple, while slower growth or higher risk often point to a lower one.

WuXi Biologics (Cayman) currently trades on a P/E of 22.60x. That compares with a Life Sciences industry average P/E of 33.86x and a peer group average of 32.57x. Simply Wall St also calculates a proprietary “Fair Ratio” for the stock of 20.00x, which is the P/E that would typically be expected given factors such as earnings growth characteristics, profit margins, industry, market cap and specific risk profile. This Fair Ratio can be more informative than simple peer or industry comparisons because it adjusts for these company specific features rather than assuming all companies deserve similar multiples. With the actual P/E sitting modestly above the Fair Ratio, the stock screens as slightly overvalued on this measure.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your WuXi Biologics (Cayman) Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you turn your view of WuXi Biologics (Cayman) into a clear story that links the business, a forecast and a fair value, then compares that fair value to the current share price to help you decide whether the stock looks attractive, fully priced or expensive to you.

On the Community page, you can see different Narratives side by side. For example, one investor might focus on WuXi Biologics (Cayman) expanding its global CRDMO and vaccine platforms with a Fair Value of HK$63.73, while another is more cautious about Western client dependence and assigns a Fair Value of HK$30.30. The platform continuously updates these Narratives when fresh earnings, guidance or news arrives so your decision framework stays aligned with the latest information rather than a static one off model.

For WuXi Biologics (Cayman), here are previews of two leading WuXi Biologics (Cayman) Narratives to help frame the range of views:

🐂 WuXi Biologics (Cayman) Bull Case

Fair Value: HK$46.39

Implied discount to this Fair Value: about 33.0% below the narrative estimate

Analyst revenue growth assumption: 16.0% a year

- Focuses on rapid growth in complex biologics such as ADCs and bispecifics, which are already a large part of the project mix.

- Highlights a broader global manufacturing footprint in Ireland, the US and Singapore that spreads regulatory and supply chain risk.

- Sees IP linked income such as royalties and milestones becoming a more important, higher margin part of the profit pool over time.

🐻 WuXi Biologics (Cayman) Bear Case

Fair Value: HK$30.30

Implied premium to this Fair Value: about 2.6% above the narrative estimate

Analyst revenue growth assumption: 14.8% a year

- Emphasises reliance on US and European clients and the risk that regulation or policy changes shift work to local suppliers.

- Flags the possibility that heavy investment in new plants could lead to lower utilisation and pressure on margins if demand softens.

- Assumes a lower future P/E multiple than today, with the stock valued closer to the more cautious end of analyst expectations.

These two narratives outline a range of reasonable outcomes that other investors are considering. The key step is to assess which set of assumptions is closer to your own view of WuXi Biologics (Cayman) and the risks you are comfortable taking.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for WuXi Biologics (Cayman) on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for WuXi Biologics (Cayman)? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English