Southern Copper (SCCO) Is Up 9.7% After Record Q1 2026 Earnings and Higher Production Guidance

- Southern Copper recently reported record net income for Q1 2026, supported by higher copper prices, low-cost operations in Peru and Mexico, and upgraded production guidance for copper, molybdenum and silver.

- Beyond the strong quarter, management’s emphasis on long-term copper demand from electrification and AI infrastructure highlights how critical new projects like Tia Maria could be to sustaining the company’s earnings and dividend profile over time.

- Next, we’ll examine how these record results and the strengthened production outlook may reshape Southern Copper’s existing investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Southern Copper Investment Narrative Recap

To own Southern Copper, you need to believe in copper’s role in electrification and AI infrastructure, and in the company’s ability to keep costs low while executing major Peru and Mexico projects. The record Q1 2026 results reinforce that story, but the near term catalyst remains progress at Tia Maria, while the biggest risk is still political and community disruption in Peru. The quarter does not remove that risk, but it strengthens the financial footing behind it.

The most relevant recent announcement here is the upgraded 2026 production guidance for copper, molybdenum and silver. That guidance ties directly into the Tia Maria and other growth projects that are central to Southern Copper’s long term volume story, and it underpins management’s confidence around earnings capacity and dividend support. For anyone watching whether the company can fund its US$15,000,000,000 capex pipeline, this higher production outlook matters.

Yet behind the record quarter, investors should also be aware of the unresolved political and community risks around key Peruvian projects like Tia Maria and Los Chancas...

Read the full narrative on Southern Copper (it's free!)

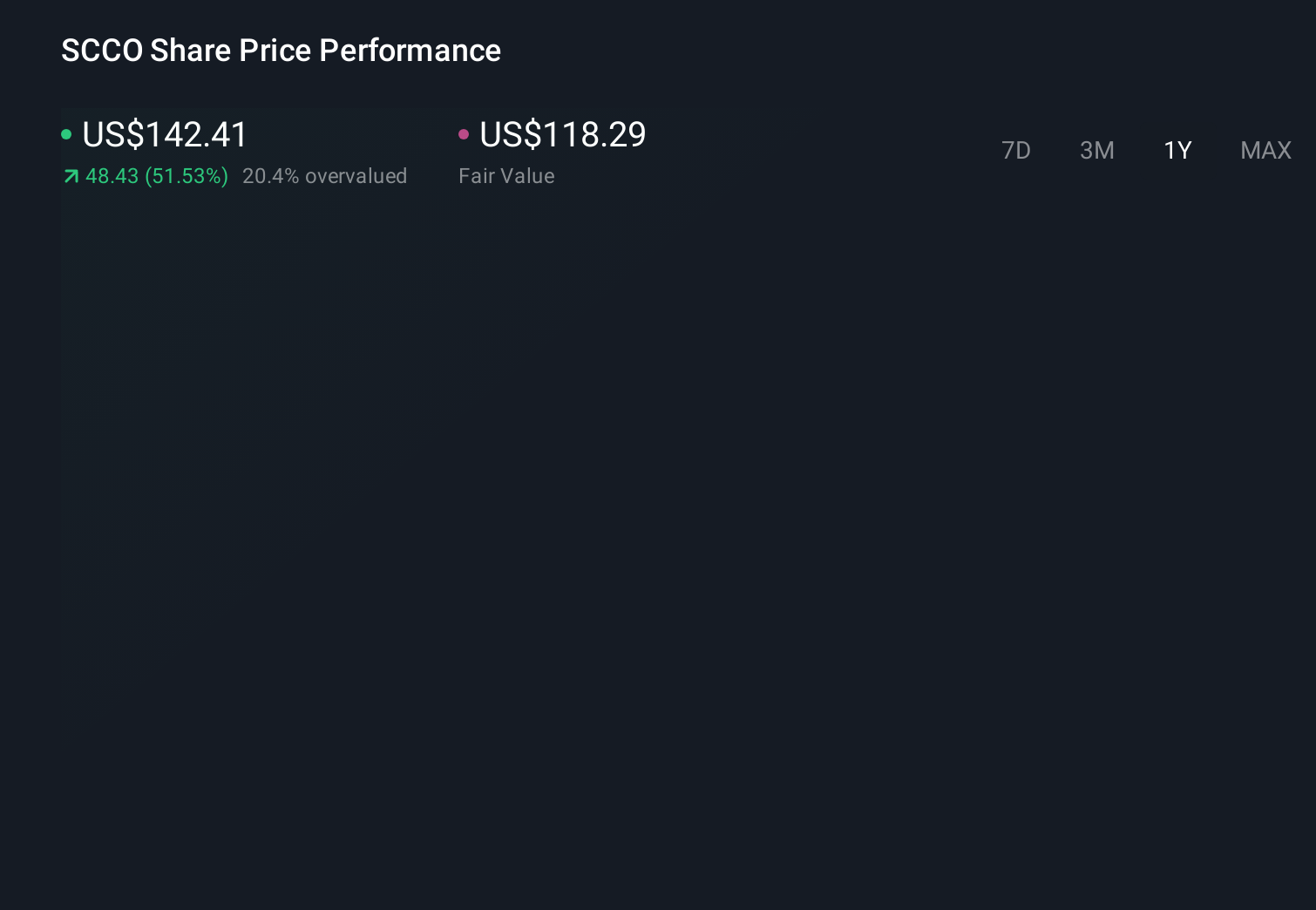

Southern Copper's narrative projects $16.5 billion revenue and $6.0 billion earnings by 2029. This requires 4.3% yearly revenue growth and a $1.0 billion earnings increase from $5.0 billion today.

Uncover how Southern Copper's forecasts yield a $163.13 fair value, a 14% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, assuming revenue could slip to about US$13,900,000,000 by 2029 and still warning that protests and permitting delays at projects like Tia Maria might offset the strong Q1 2026 results, which shows how differently you and other shareholders can interpret the same set of facts.

Explore 4 other fair value estimates on Southern Copper - why the stock might be worth 43% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southern Copper research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English