Ultra Clean Holdings (UCTT) Stock After Strong Q1 Beat Is The Valuation Getting Ahead Of Itself

Ultra Clean Holdings (UCTT) has been in focus after reporting first quarter results that exceeded analyst expectations on both revenue and earnings, supported by favorable research commentary and sector-wide strength in semiconductor equipment stocks.

See our latest analysis for Ultra Clean Holdings.

Recent price action has been strong, with a 32.69% 7 day share price return, a 95.44% 90 day share price return and a 298.61% year to date share price return. The 1 year total shareholder return is also very large, suggesting momentum has built quickly around Ultra Clean’s role in the semiconductor equipment cycle.

If you are watching how AI linked semiconductor demand is moving capital, this is a useful moment to look beyond UCTT and check out 48 AI infrastructure stocks

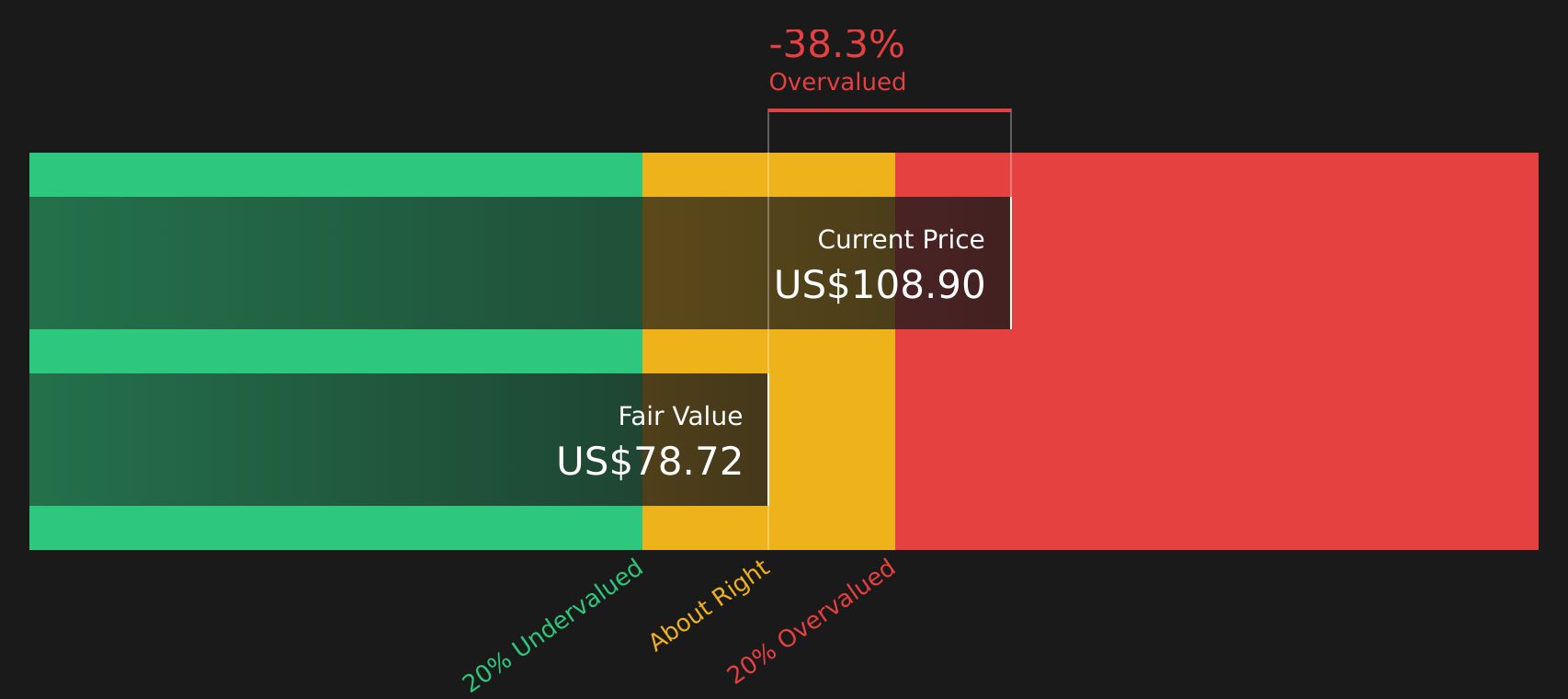

With UCTT now trading around US$108.90, just above one major analyst target of US$107.40 and after very strong recent returns, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 4.3% Overvalued

Ultra Clean Holdings last closed at $108.90 while the most followed narrative pegs fair value at $104.40, so the market price currently sits a little above that estimate.

Diversification efforts, including expansion of the Services business and integration of acquired units (Fluid Solutions, Services, HIS), are expected to reduce customer concentration risk and provide more stable, incremental revenue streams even as wafer fab investment cycles remain volatile. This impacts revenue stability and reduces downside earnings risk.

Curious what sits behind that fair value call? The narrative leans on faster revenue growth, firmer margins and a richer earnings multiple than the stock has today.

Result: Fair Value of $104.40 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points to watch, including dependence on a small group of large customers and ongoing tariff related costs that could weigh on margins.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Paint A Different Picture

While the most followed narrative points to UCTT being about 4.3% overvalued on a fair value of $104.40, the SWS DCF model comes out more cautious, with an estimate of $78.72. That gap suggests investors need to weigh how much optimism is already in today’s $108.90 price.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Given the mix of optimism and caution in this story, it makes sense to review the underlying data now and decide where you stand. To see both sides of the debate in one place, start with the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you could miss other opportunities that better match your goals, risk comfort and income needs.

- Hunt for value by scanning companies that combine quality fundamentals with attractive pricing using the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks identified as potential 8 dividend fortresses.

- Prioritise resilience by checking companies highlighted in the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English