Reverse Split and Governance Shift Could Be A Game Changer For Marqeta (MQ)

- At its 2026 Annual Meeting held on June 10, Marqeta, Inc. approved a 1-for-4 reverse stock split, reduced its authorized common and preferred shares, and amended its certificate of incorporation to allow officer exculpation under Delaware law.

- This combination of capital structure adjustments and expanded officer protections marks a meaningful shift in how Marqeta manages both its share base and governance risk.

- Next, we'll explore how the 1-for-4 reverse stock split and governance changes could influence Marqeta's existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Marqeta Investment Narrative Recap

To own Marqeta, you need to believe its card issuing platform can stay relevant as embedded finance and digital payments expand, while customer concentration and competition remain manageable. The 1-for-4 reverse split and governance changes mainly tidy up the capital structure and legal framework, and do not materially change the near term focus on execution with key clients or the concentration risk around large accounts.

The recent expansion of Marqeta’s account and money movement tools across 30 additional European countries is closely tied to this. It reinforces the core catalyst of broader international usage of its platform, which could matter more for the story than the mechanics of the reverse split itself, especially as investors watch how new European capabilities interact with existing reliance on a handful of major customers.

Yet, while these changes may look incremental, the concentration risk around a few key clients is something investors should be aware of...

Read the full narrative on Marqeta (it's free!)

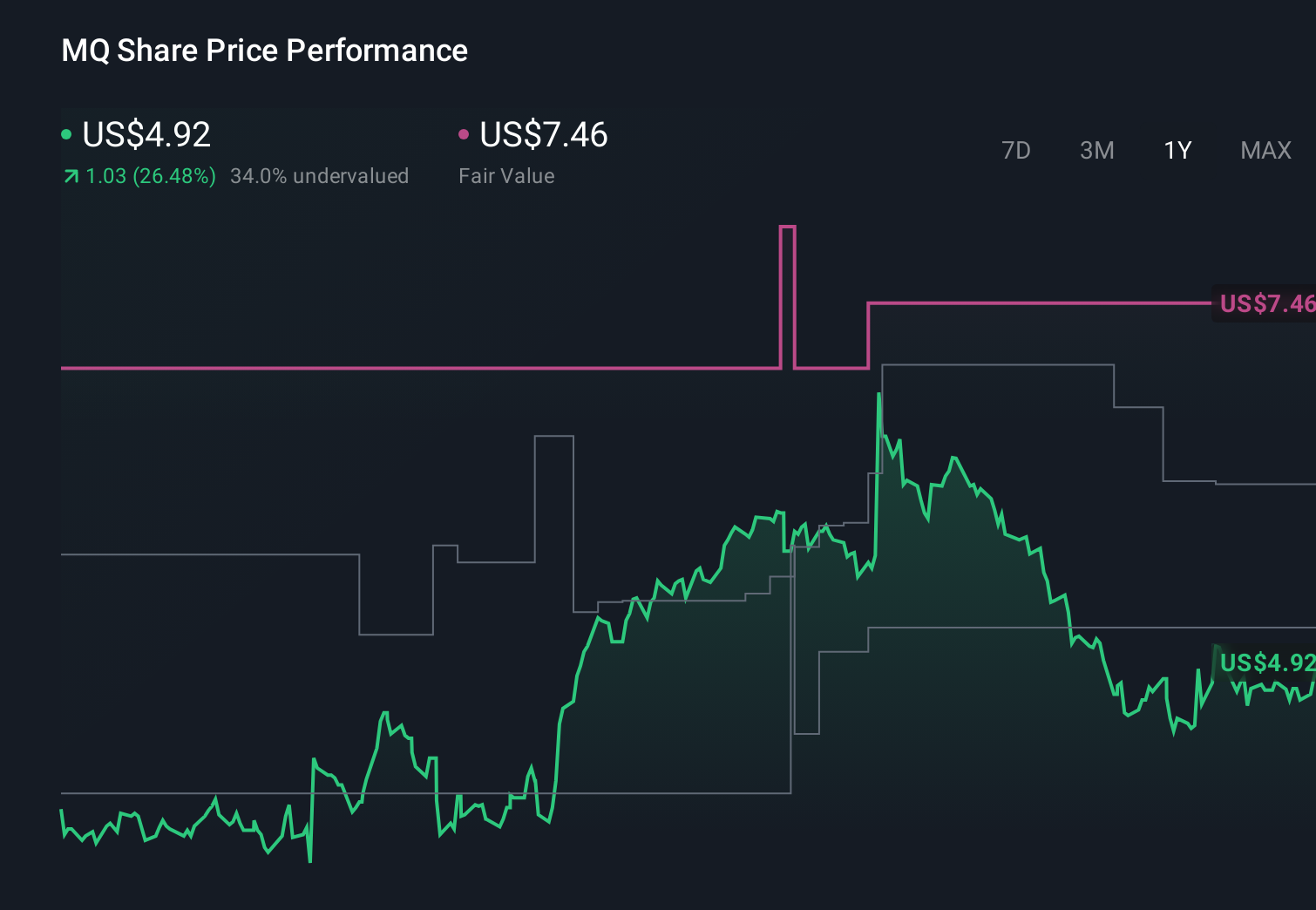

Marqeta's narrative projects $969.0 million revenue and $73.1 million earnings by 2029. This requires 14.1% yearly revenue growth and a roughly $71 million earnings increase from $2.2 million today.

Uncover how Marqeta's forecasts yield a $5.19 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts once projected Marqeta reaching about US$1.0 billion in revenue and US$194.5 million in earnings by 2028, highlighting how views on European expansion and client wins can differ sharply. You may see the reverse split and governance tweaks as either reinforcing that upside story or as reasons to revisit whether those bullish assumptions still fit your own expectations.

Explore 3 other fair value estimates on Marqeta - why the stock might be worth as much as 78% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English