3 Asian Stocks Estimated To Be Trading At Discounts Of Up To 29.4%

As global markets navigate through heightened inflation pressures and geopolitical tensions, Asian equities present a complex landscape with both challenges and opportunities. In this environment, identifying undervalued stocks can be particularly appealing for investors seeking to capitalize on potential discounts; these stocks often exhibit strong fundamentals or growth prospects that are not yet fully reflected in their current prices.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| TRIAL Holdings (TSE:141A) | ¥2789.00 | ¥5491.20 | 49.2% |

| Strike Group (TSE:6196) | ¥1262.00 | ¥2447.05 | 48.4% |

| Precision Tsugami (China) (SEHK:1651) | HK$52.45 | HK$103.96 | 49.5% |

| Pegasus (TSE:6262) | ¥512.00 | ¥1008.12 | 49.2% |

| Moshi Moshi Retail Corporation (SET:MOSHI) | THB36.75 | THB71.34 | 48.5% |

| Innovent Biologics (SEHK:1801) | HK$76.45 | HK$152.88 | 50% |

| Cybozu (TSE:4776) | ¥2293.00 | ¥4513.60 | 49.2% |

| China XLX Fertiliser (SEHK:1866) | HK$10.11 | HK$20.17 | 49.9% |

| APR (KOSE:A278470) | ₩394000.00 | ₩769987.44 | 48.8% |

| Alltop Technology (TPEX:3526) | NT$323.00 | NT$629.99 | 48.7% |

Let's uncover some gems from our specialized screener.

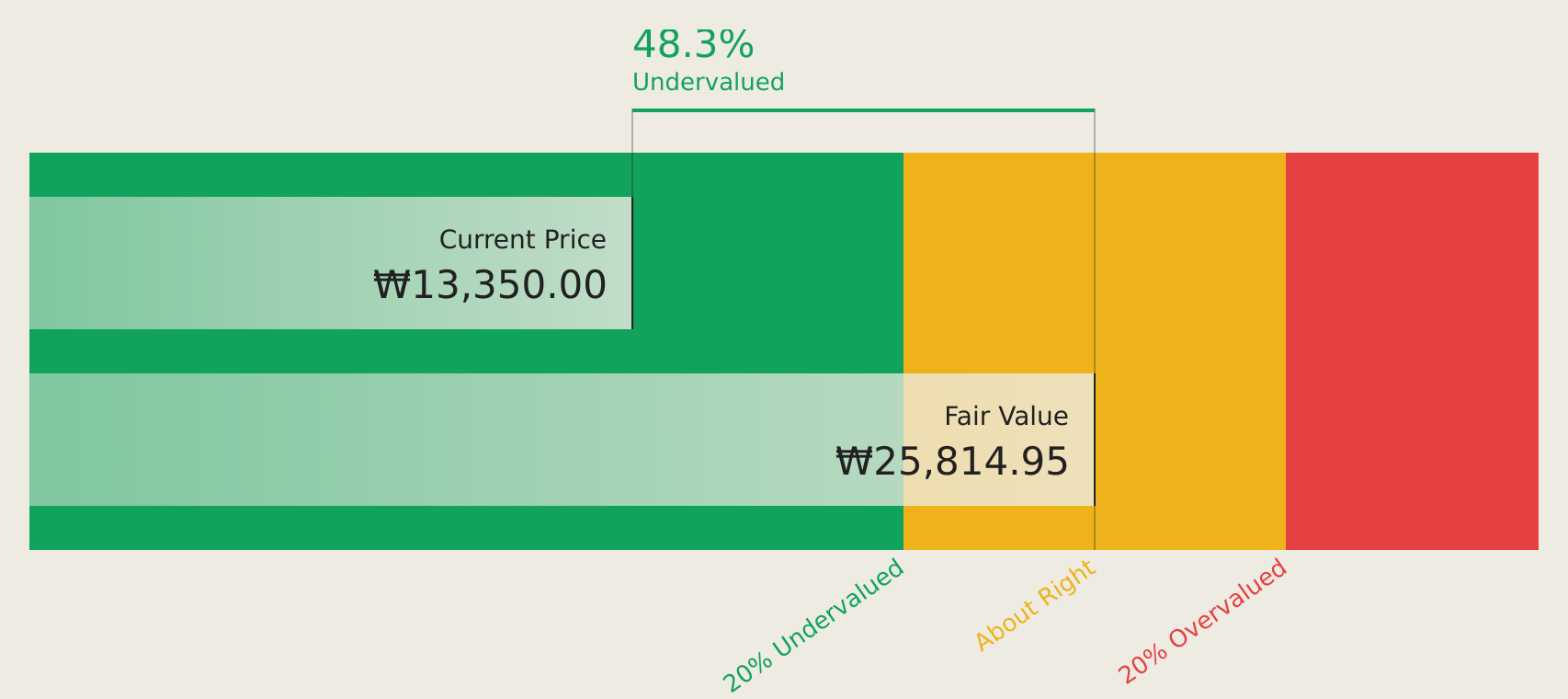

NC Chem (KOSDAQ:A482630)

Overview: NC Chem Corporation specializes in producing and selling fine chemical materials for semiconductors in South Korea, with a market capitalization of approximately ₩380.86 billion.

Operations: NC Chem's revenue primarily comes from the production and sale of fine chemical materials used in the semiconductor industry within South Korea.

Estimated Discount To Fair Value: 27.1%

NC Chem is trading at ₩17,400, significantly below its estimated future cash flow value of ₩23,868.47. This indicates it is highly undervalued based on discounted cash flow analysis. The company’s revenue is forecast to grow by 20.3% annually, outpacing the Korean market's average growth rate of 16.2%. However, despite strong earnings growth of 52.1% last year and expected annual profit growth above 20%, its return on equity remains low at a forecasted 19.3%.

- Our earnings growth report unveils the potential for significant increases in NC Chem's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of NC Chem.

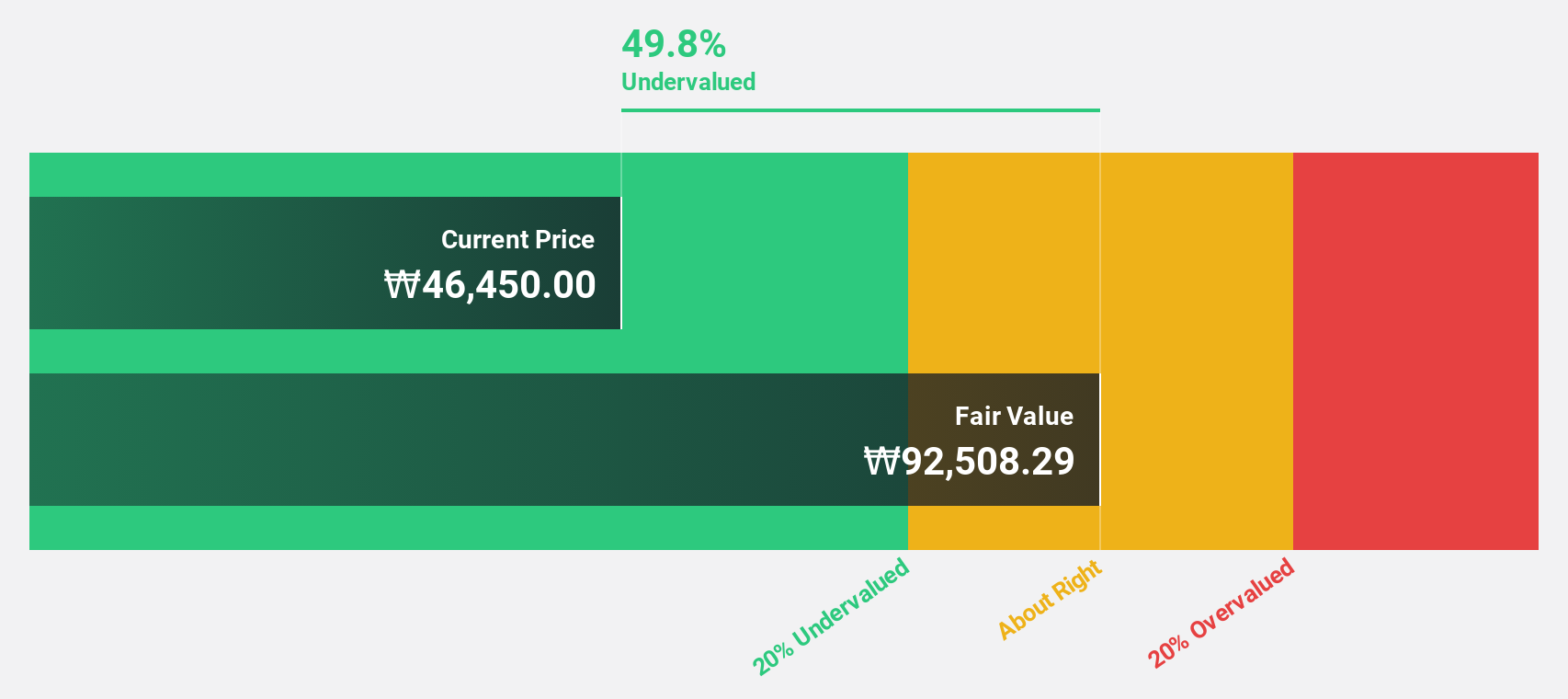

ISU Petasys (KOSE:A007660)

Overview: ISU Petasys Co., Ltd. manufactures and sells printed circuit boards (PCBs) with a market cap of ₩8.99 trillion.

Operations: ISU Petasys generates revenue through the production and sale of printed circuit boards (PCBs).

Estimated Discount To Fair Value: 14.4%

ISU Petasys, currently priced at ₩122,400, trades 14.4% below its estimated future cash flow value of ₩143,056.25. The company shows robust earnings growth of 82.1% over the past year and is forecast to maintain a high annual profit growth rate of 38%, surpassing the Korean market's average. However, its share price has been highly volatile recently and it features a high level of non-cash earnings which might affect quality assessments.

- Our expertly prepared growth report on ISU Petasys implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of ISU Petasys here with our thorough financial health report.

East Buy Holding (SEHK:1797)

Overview: East Buy Holding Limited is an investment holding company that operates a livestreaming e-commerce business for sales of private label products in the People's Republic of China, with a market cap of HK$22.89 billion.

Operations: The company generates revenue primarily through its online live commerce business, amounting to CN¥4.52 billion.

Estimated Discount To Fair Value: 29.4%

East Buy Holding, priced at HK$21.72, is trading over 29% below its estimated future cash flow value of HK$30.75, indicating potential undervaluation. The company recently initiated a share buyback program to enhance net asset value and earnings per share. Despite low forecasted return on equity (9%), East Buy's earnings are expected to grow significantly at 24.7% annually, outpacing the Hong Kong market average of 12.6%, although revenue growth remains moderate at 15.8%.

- In light of our recent growth report, it seems possible that East Buy Holding's financial performance will exceed current levels.

- Unlock comprehensive insights into our analysis of East Buy Holding stock in this financial health report.

Make It Happen

- Explore the 176 names from our Undervalued Asian Stocks Based On Cash Flows screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English