3 Reasons to Sell PHM and 1 Stock to Buy Instead

PulteGroup has been treading water for the past six months, recording a small return of 1.1% while holding steady at $122.97. The stock also fell short of the S&P 500’s 10.9% gain during that period.

Is there a buying opportunity in PulteGroup, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is PulteGroup Not Exciting?

We’re cautious about PulteGroup. Here are three reasons why PHM doesn’t excite us, plus one stock we’d rather own.

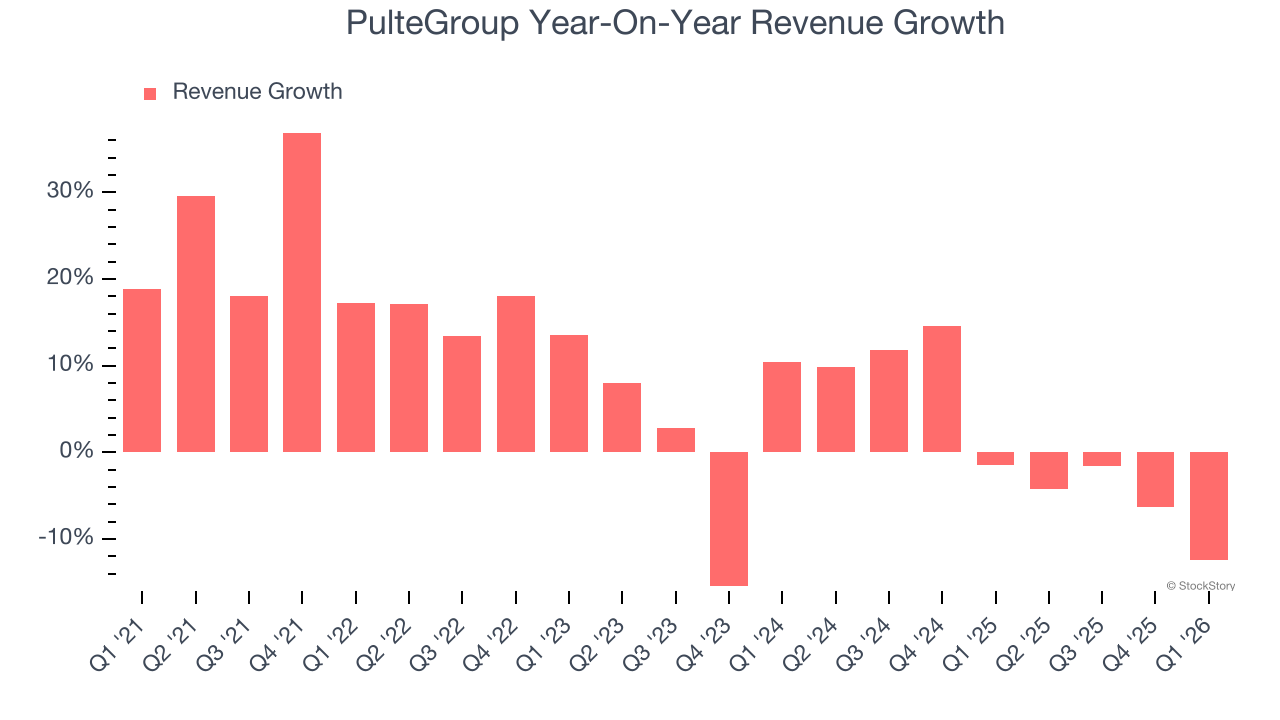

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. PulteGroup’s recent performance shows its demand has slowed as its annualized revenue growth of 1.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

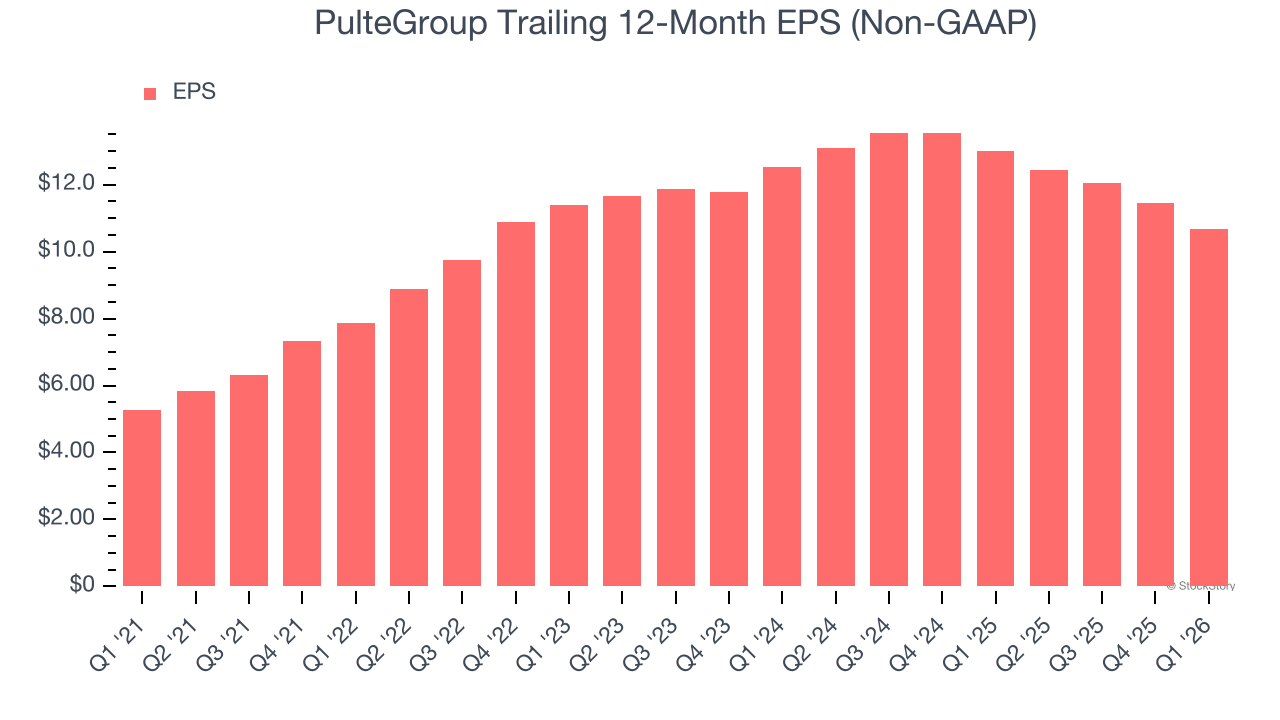

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for PulteGroup, its EPS declined by 7.7% annually over the last two years while its revenue grew by 1.2%. This tells us the company became less profitable on a per-share basis as it expanded.

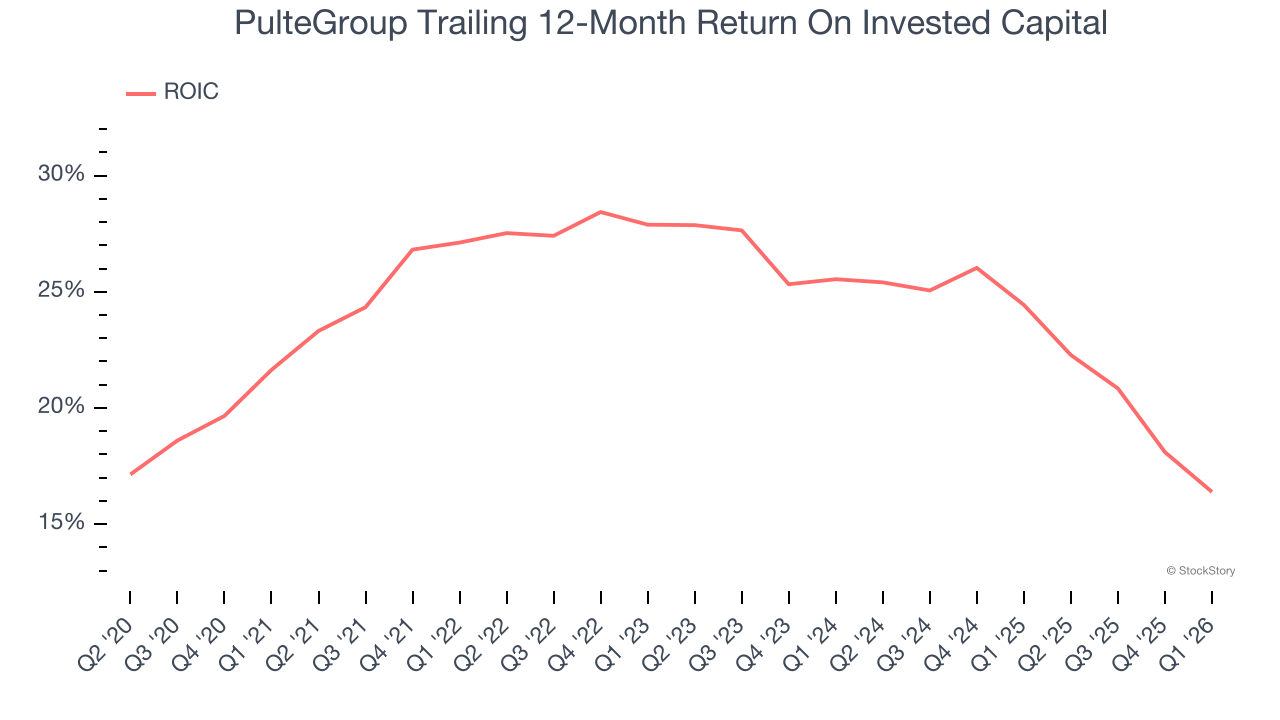

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

Unfortunately, PulteGroup’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

PulteGroup isn’t a terrible business, but it doesn’t pass our bar. With its shares lagging the market recently, the stock trades at 12.2× forward P/E (or $122.97 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re fairly confident there are better investments elsewhere. Let us point you toward the Amazon and PayPal of Latin America.

Stocks We Like More Than PulteGroup

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English