Are Macro Jitters Exposing a Hidden Fragility in Photronics’ (PLAB) Semiconductor-Sector Narrative?

- In recent days, Photronics, a photomask supplier to the semiconductor industry, has come under pressure as chip-related stocks reacted to macroeconomic concerns and survey data showing semiconductors as one of the most crowded trades.

- This episode highlights how sentiment-driven sector swings and interest-rate expectations can influence Photronics’ outlook, even when there is little company-specific news.

- We’ll now examine how this sector-wide, sentiment-driven pressure on semiconductor names affects Photronics’ existing investment narrative and risk profile.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

Photronics Investment Narrative Recap

To own Photronics, you have to believe that demand for its photomasks across IC and display markets will support ongoing investment in advanced capacity, even through sector volatility. The recent sentiment-driven selloff in semiconductor stocks does not materially change Photronics’ near term catalyst of executing on its technology upgrades, but it does underline the key risk that cyclical swings and crowding in chip trades can amplify short term price and earnings uncertainty.

The most relevant recent update here is Photronics’ Q3 2026 outlook, guiding revenue to US$207 million to US$215 million with an 18% to 20% operating margin target. Against the backdrop of a sector pullback and concerns over crowded semiconductor positioning, this guidance frames how well Photronics’ operations and cost discipline could buffer sentiment-driven pressures while it continues to invest heavily in advanced tooling and capacity.

Yet while the share price reaction may feel temporary, investors should be aware that shorter order visibility and cyclical design volatility can...

Read the full narrative on Photronics (it's free!)

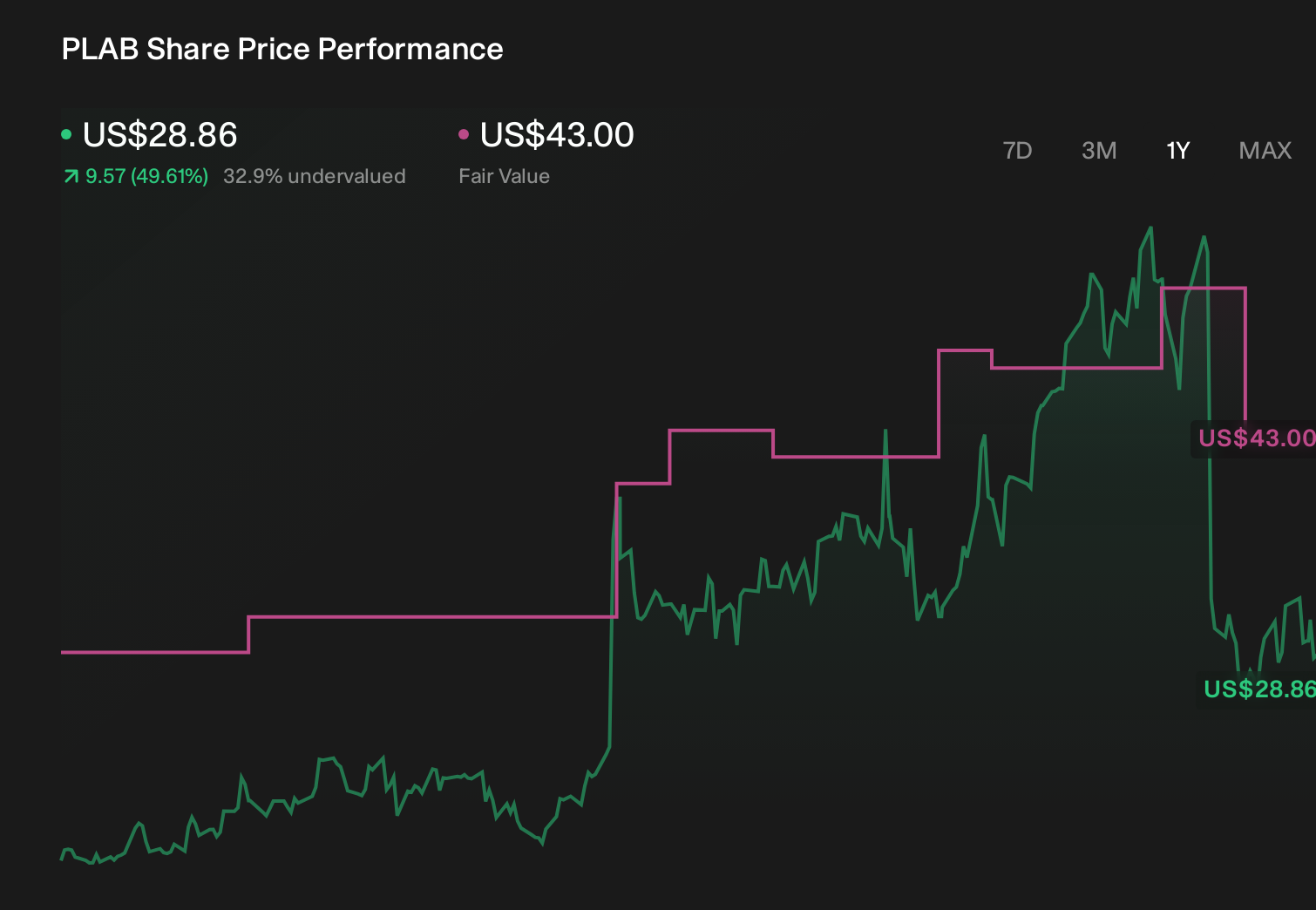

Photronics' narrative projects $930.0 million revenue and $81.2 million earnings by 2029. This requires 2.6% yearly revenue growth and a $77.9 million earnings decrease from $159.1 million today.

Uncover how Photronics' forecasts yield a $43.00 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently see fair value for Photronics between US$21.70 and US$43.00, underscoring how widely opinions can differ. As you weigh these views against the risk of unpredictable quarterly swings tied to sector sentiment, it can be useful to compare several contrasting assessments before deciding how Photronics might fit into your own expectations for semiconductor demand and company specific execution.

Explore 5 other fair value estimates on Photronics - why the stock might be worth as much as 28% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English