The Bull Case For Plexus (PLXS) Could Change Following Its Expanded Long-Term Credit Facility - Learn Why

- Plexus Corp. recently entered into a Second Amended and Restated Credit Agreement with JPMorgan Chase and other lenders, replacing its 2022 facility with a revolving credit line maturing in June 2031 and commitments that can rise from US$500 million to as much as US$750 million.

- This longer-dated, expandable credit facility with interest and fee terms tied to Plexus’s leverage and interest coverage ratios may meaningfully influence its financial flexibility and risk profile.

- We’ll now examine how this extended, expandable credit facility shapes Plexus’s existing investment narrative around growth capacity and balance sheet strength.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Plexus Investment Narrative Recap

To own Plexus, you need to believe in its role as a partner for complex, high value electronics across healthcare, industrial and aerospace and defense, supported by disciplined balance sheet management. The new, longer term revolving credit facility modestly improves Plexus’s liquidity and acquisition capacity, but does not fundamentally change the near term narrative, where execution on program ramps remains a key catalyst and concentrated customer demand and sector cyclicality still stand out as the biggest risks.

The recent Riverside Research partnership in defense and intelligence hardware is especially relevant here, because it highlights the kind of complex, security focused programs Plexus may look to support with its expanded credit capacity. As these types of programs scale, they can be sensitive to order timing and budget decisions, so the combination of a stronger liquidity backstop and program driven exposure will be important for investors to monitor together.

Yet beneath the reassuring headline of more credit capacity, investors should still be aware that revenue remains heavily exposed to a handful of large customers and sector specific swings...

Read the full narrative on Plexus (it's free!)

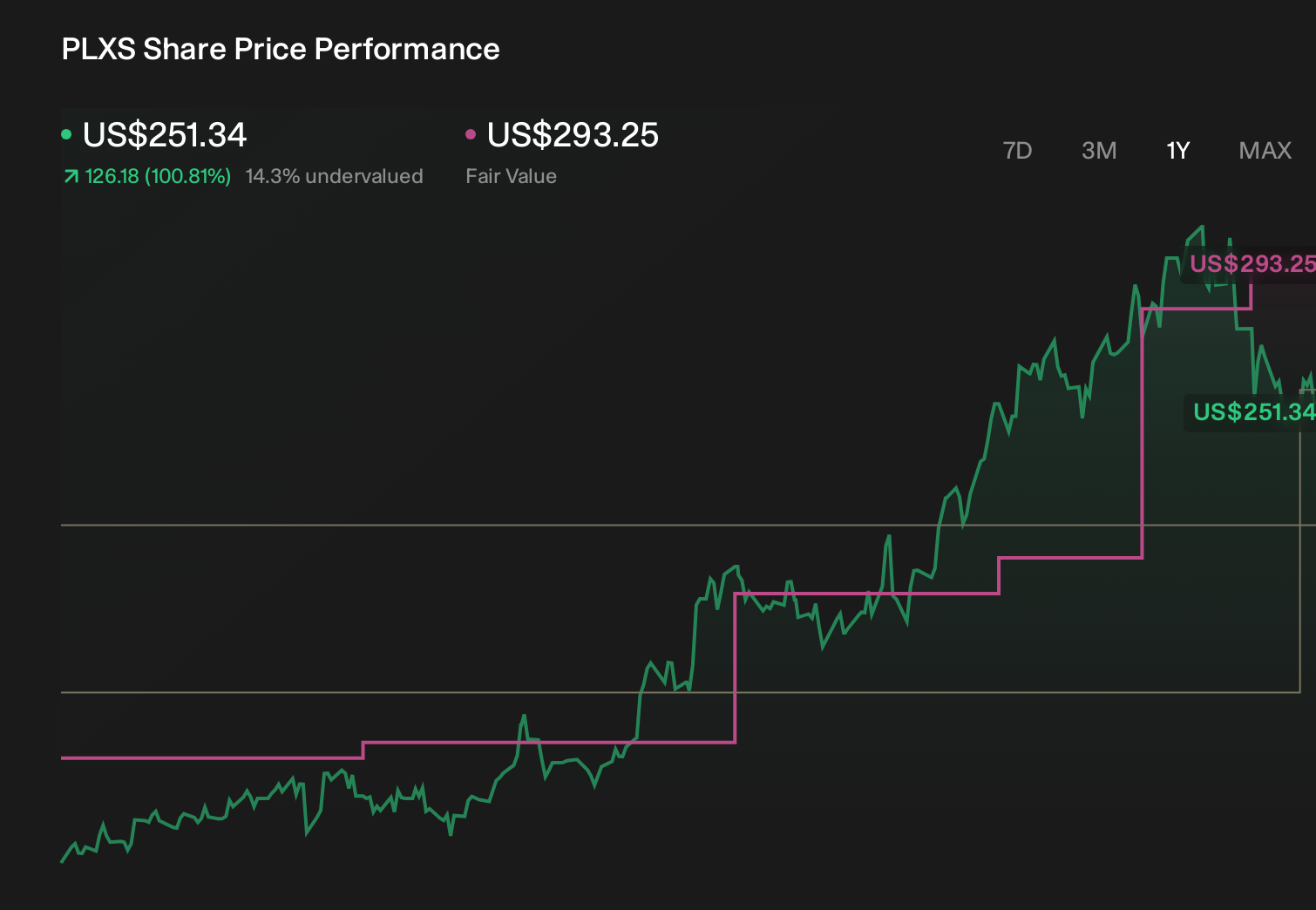

Plexus' narrative projects $6.0 billion revenue and $278.4 million earnings by 2029. This requires 11.8% yearly revenue growth and an earnings increase of about $90.9 million from $187.5 million today.

Uncover how Plexus' forecasts yield a $280.75 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue of about US$5.2 billion and earnings of roughly US$257 million by 2029, so if you lean toward that more upbeat view, this larger, longer dated credit facility could either reinforce your expectations for capital fueled growth or prompt you to reassess how much balance sheet risk you are comfortable with.

Explore 2 other fair value estimates on Plexus - why the stock might be worth 49% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Plexus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Plexus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Plexus' overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English