How Investors May Respond To PDF Solutions (PDFS) Profit Surge And Revenue Growth In A Hotter Chip Sector

- In recent days, PDF Solutions reported a strong improvement in its financial profile, including a very large net profit increase and double‑digit revenue growth, alongside positive technical indicators for its shares within a broadly upbeat semiconductor sector.

- This combination of healthier fundamentals, sector enthusiasm, and technically driven interest has sharpened investor focus on how the company’s analytics and software capabilities fit into the semiconductor manufacturing ecosystem.

- We’ll now examine how this recent jump in revenue and profitability could influence PDF Solutions’ existing investment narrative and risk‑reward balance.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

PDF Solutions Investment Narrative Recap

To own PDF Solutions, you need to believe that its analytics and software will stay central to how chip makers improve yield and efficiency, supporting a shift toward higher quality, recurring revenue. The recent jump in revenue and profitability strengthens that case in the near term, but the sharp move in the share price also amplifies valuation risk as a key short term concern, especially if growth expectations or sector sentiment cool.

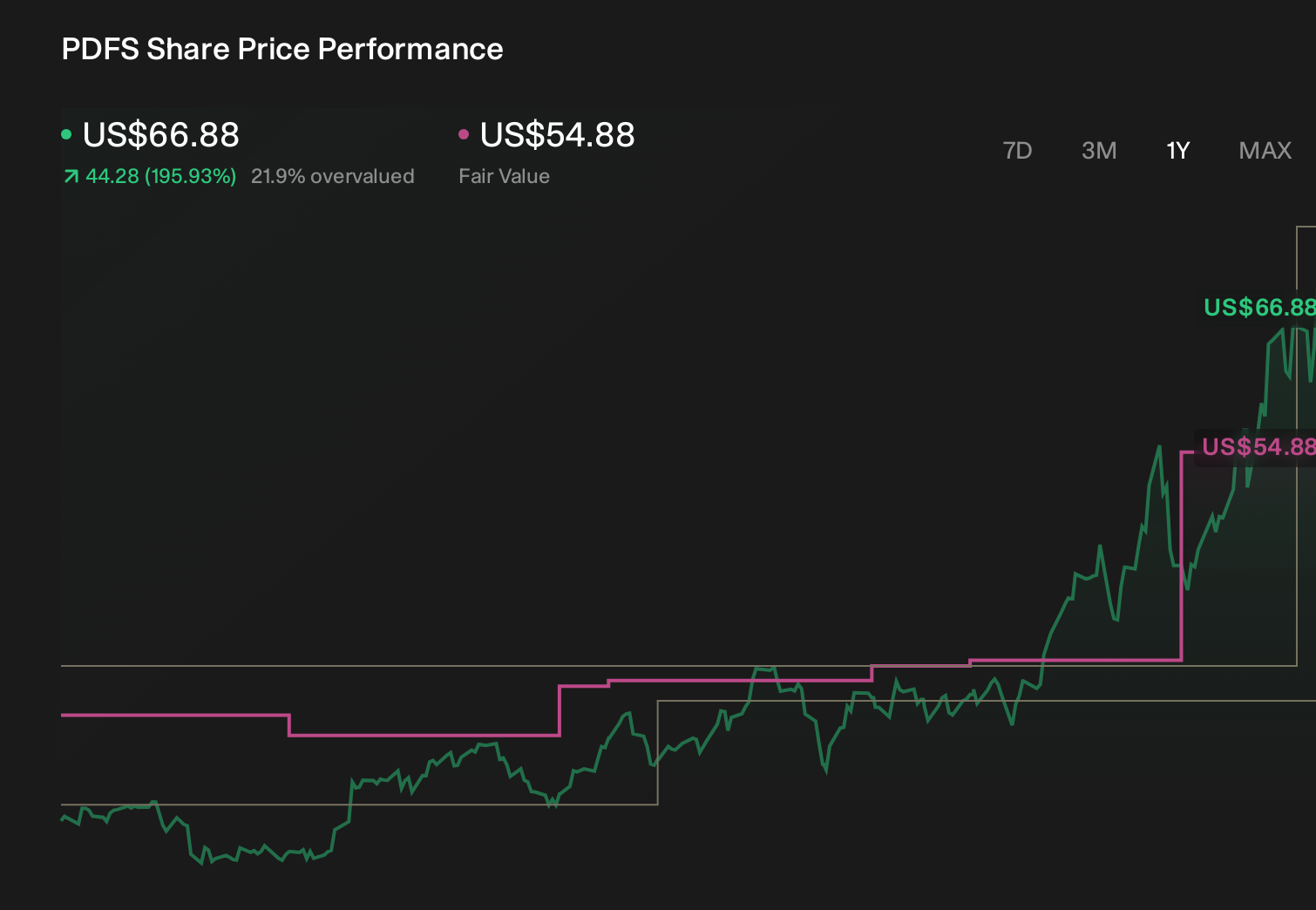

The Q1 2026 results are the most relevant development here: revenue grew to US$60.13 million with net income of US$4.79 million, reversing last year’s loss and contributing to a 25.85% year over year revenue increase and a 258.01% net profit increase. This improved financial profile sits alongside buoyant sector conditions and strong technical signals, potentially reinforcing confidence in PDF Solutions’ SaaS and analytics adoption catalyst while also intensifying debate about how much optimism is already reflected in the share price.

Yet against this stronger near term picture, investors should still pay close attention to how concentrated customer relationships could affect...

Read the full narrative on PDF Solutions (it's free!)

PDF Solutions’ narrative projects $383.8 million revenue and $84.0 million earnings by 2029.

Uncover how PDF Solutions' forecasts yield a $54.88 fair value, a 16% downside to its current price.

Exploring Other Perspectives

While current results look strong, the most pessimistic analysts were assuming revenue of about US$378.5 million and earnings of roughly US$50.8 million by 2029, reminding you that some worry customer concentration and stricter data rules could leave today’s optimism looking fragile if conditions or expectations shift.

Explore 4 other fair value estimates on PDF Solutions - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your PDF Solutions research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free PDF Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PDF Solutions' overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English