Owens Corning (OC) Stock Could Be 11.5% Undervalued After Earnings Beat And 2026 Outlook

Owens Corning (OC) is back in focus after declaring a quarterly cash dividend of $0.79 per share, along with earnings that exceeded expectations and an updated fiscal 2026 outlook that investors are watching closely.

See our latest analysis for Owens Corning.

The recent dividend declaration and earnings beat come on top of a strong run in Owens Corning’s share price, with a 30 day share price return of 10.41% and a 90 day return of 28.19%. This is occurring even though the 1 year total shareholder return is slightly negative at 0.40%, and longer term total shareholder returns over 3 and 5 years, at 9.24% and 44.93% respectively, remain positive. This suggests momentum has picked up recently as investors react to the improved 2026 outlook and rising institutional ownership, while also weighing recent insider selling.

If Owens Corning’s recent move has you looking for other ideas in related areas, it could be worth scanning 34 power grid technology and infrastructure stocks as another way to find infrastructure linked opportunities.

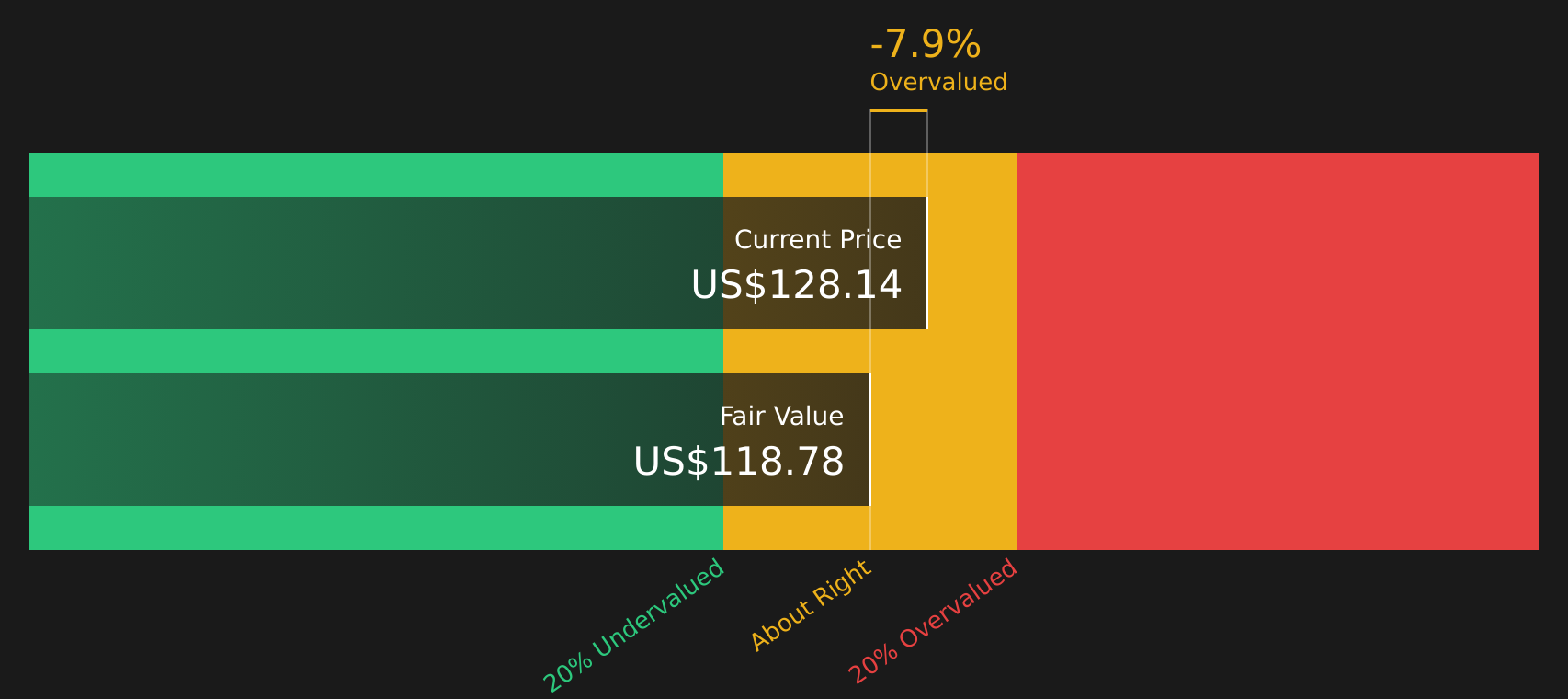

With Owens Corning trading at $128.14 and some valuation models tagging the stock as modestly undervalued, the key question now is simple: is there still an opportunity for investors to consider here, or is the market already fully accounting for expectations about future growth?

Most Popular Narrative: 11.5% Undervalued

Owens Corning is trading at $128.14, while the most followed narrative pegs fair value at $144.80, using a 10.07% discount rate to frame the long term opportunity.

Robust, forward investment in capacity expansion and technology, including new shingle and nonwovens lines, positions Owens Corning to capture increasing demand for energy-efficient, resilient building materials, supporting future revenue growth as energy codes tighten and consumer preferences shift towards sustainable construction.

Want to see what sits behind that valuation gap? The narrative leans heavily on future revenue, margin uplift, and a compressed earnings multiple. The exact mix may surprise you.

Result: Fair Value of $144.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Owens Corning’s narrative could be knocked off course if weakness in North American housing related demand persists, or if oversupplied roofing and insulation markets pressure pricing and margins.

Find out about the key risks to this Owens Corning narrative.

Another View: Owens Corning Through A Cash Flow Lens

While the leading Owens Corning narrative sees around 11.5% upside to a fair value of $144.80, our DCF model points in the other direction. In this view, OC at $128.14 is trading above an estimated future cash flow value of $118.78, which implies less of a margin of safety than the narrative suggests. For investors, that raises a simple question: which set of assumptions feels more realistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Owens Corning for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Owens Corning attracting both optimism and concern, it makes sense to review the numbers yourself and move quickly to form a balanced view. To see how current risks and rewards line up in one place, take a closer look at the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Owens Corning?

Do not stop with Owens Corning. Broaden your watchlist now using focused stock ideas that could sharpen your next move and help you act before others do.

- Target income potential by reviewing resilient high yield opportunities in the 8 dividend fortresses.

- Hunt for quality at a discount by scanning the 45 high quality undervalued stocks that combine solid fundamentals with attractive pricing.

- Spot future standouts early by checking the screener containing 19 high quality undiscovered gems before they land firmly on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English