Simpson Manufacturing (SSD) Stock Could Be 8.1% Undervalued After Housing Data And Earnings Strength

Simpson Manufacturing (SSD) stock moved higher after U.S. pending home sales improved and mortgage rates eased slightly, which lifted housing affordability and trading interest just as the company reports higher revenue and net profit.

See our latest analysis for Simpson Manufacturing.

The latest move builds on a broader positive pattern for Simpson Manufacturing, with a 1 month share price return of 8.4% and year to date share price return of 21.5%. The 1 year total shareholder return of 31.1% and 5 year total shareholder return of 89.2% point to momentum that has been supported by higher revenue, rising net profit and stronger institutional interest, even as recent housing data and a new Corporate Social Responsibility report keep the stock in focus.

If you are looking for other construction exposed opportunities as housing data improves, it could be a useful moment to check out 34 power grid technology and infrastructure stocks

With Simpson Manufacturing reporting rising revenue and net profit, a strong recent share price run, and an 8.8% gap to the average analyst price target near $217.80, the key question is whether there is still an opportunity or if the stock already reflects expectations for future growth.

Most Popular Narrative: 8.1% Undervalued

With Simpson Manufacturing last closing at $200.14 against a narrative fair value of $217.80, the current pricing sits below what the most followed model suggests, putting the recent share price strength in a different light for investors tracking this story.

The accelerating adoption of off-site, modular, and mass timber construction solutions is creating significant demand for high-performance, engineered fasteners and connectors, an area where Simpson continues to see double-digit OEM volume growth and increasing traction with new digital and software solutions. This is likely to support above-market revenue growth.

Want to see what sits behind that fair value for Simpson Manufacturing? The core of this narrative is moderate revenue growth, firmer margins and a richer future earnings multiple. Curious which combination of earnings forecasts and valuation assumptions needs to hold for that target to stack up?

Result: Fair Value of $217.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Simpson Manufacturing still faces pressure from housing cycles and steel tariffs; weaker construction activity or sustained input cost inflation could quickly test the current valuation narrative.

Find out about the key risks to this Simpson Manufacturing narrative.

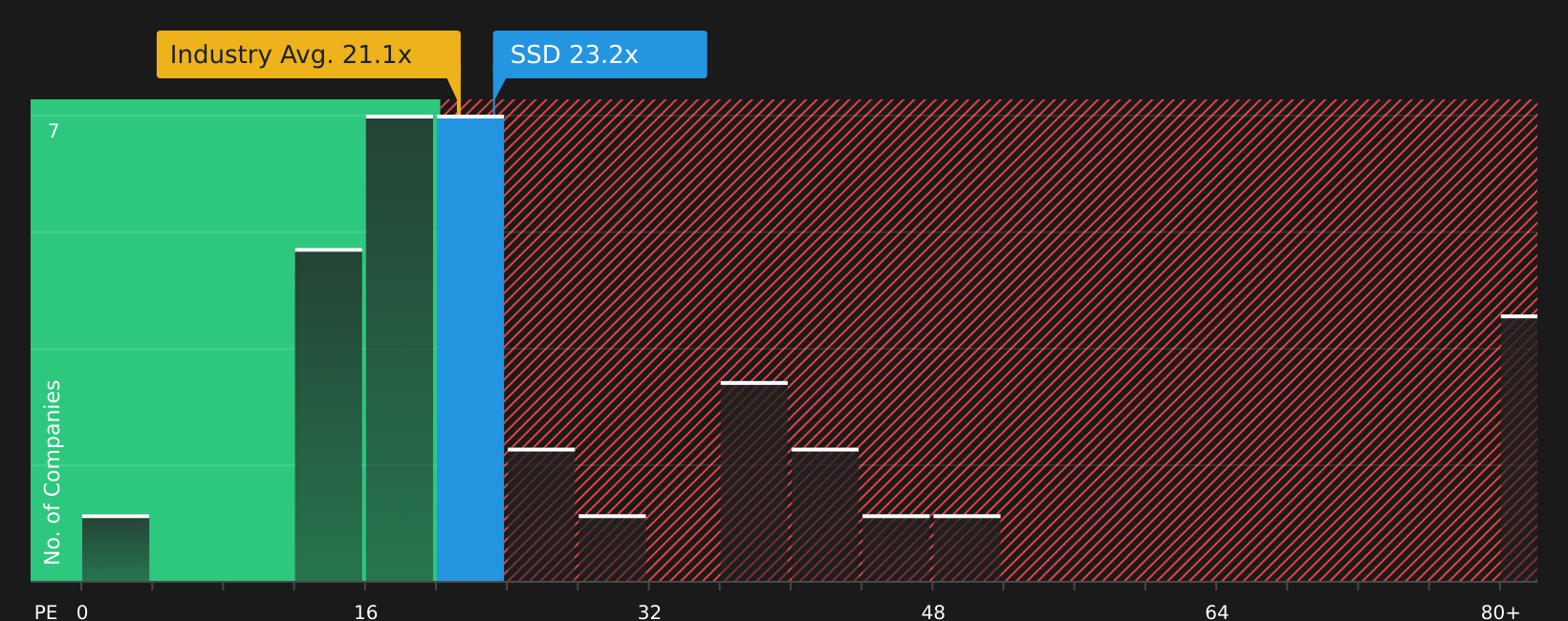

Another View: Simpson Manufacturing Through a P/E Lens

The SWS narrative suggests Simpson Manufacturing is trading below a fair value of $217.80, yet the P/E ratio of 23.2x sits above the US Building industry at 21.1x and slightly above the 22.7x fair ratio. That premium hints at less margin for error, so which signal should matter more to you?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment leaning constructive around Simpson Manufacturing, it could be worth reviewing the numbers yourself and deciding how convincing the story really looks. To understand what optimists are focusing on, start with the 2 key rewards

Looking for more investment ideas beyond Simpson Manufacturing?

Before you move on, consider giving yourself the chance to spot fresh opportunities that match your style by using a few targeted stock screeners from Simply Wall St.

- Boost your search for quality by checking companies that combine attractive valuations with solid fundamentals through the 45 high quality undervalued stocks.

- Prioritise resilience by focusing on companies with strong financial footing using the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for under-the-radar opportunities that others might be overlooking by reviewing the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English