Oceaneering International (OII) Stock Could Be 2.3% Overvalued After BlackRock Backing And Stronger Results

Institutional buying and improving fundamentals put Oceaneering International in focus

Oceaneering International (OII) is drawing fresh attention after BlackRock and State Street increased their positions, alongside year-over-year gains in quarterly revenue and net profit and a solid financial health score within its industry.

For you as an investor, this mix of stronger institutional interest and improving reported fundamentals sits against ongoing concerns about operating efficiency and longer term sales trends. This sets up a more nuanced risk reward profile for the stock.

See our latest analysis for Oceaneering International.

At a share price of US$36.06, Oceaneering International has seen a 45.11% year to date share price return and a 68.98% total shareholder return over the past year. More recent one month and one week share price returns have cooled, which suggests strong longer term momentum alongside some short term consolidation as investors assess the higher institutional ownership and valuation signals.

If you are comparing Oceaneering International with other industrial robotics and automation plays, this is a good moment to scan the market using our 31 robotics and automation stocks

With Oceaneering International trading near its analyst price target and showing only a modest intrinsic discount, its strong recent returns and rising institutional ownership raise a key question: is there still value on the table, or is the market already pricing in future growth?

Most Popular Narrative: 2.3% Overvalued

With Oceaneering International last closing at $36.06 against a narrative fair value of $35.25, the most followed valuation view sees the stock as slightly ahead of its modeled worth, and that hinges heavily on how its traditional energy exposure and newer segments evolve.

The ongoing global energy transition and intensifying decarbonization efforts continue to limit new offshore oil & gas developments, which threatens Oceaneering's long-term project backlog and could ultimately reduce future revenue growth as the addressable market gradually contracts.

There is increasing investor and regulatory pressure to reallocate capital away from traditional oilfield service providers; this trend is likely to hinder capital flows to Oceaneering's core business lines, potentially compressing growth prospects, restraining order activity, and constraining revenue and profit expansion.

Want to understand why a company with rising recent earnings is modeled for shrinking profits, modest revenue growth, and a much richer future earnings multiple than today? The full narrative walks through how these assumptions connect into one cohesive valuation story and what has to go right for that pricing to hold.

Result: Fair Value of $35.25 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if Oceaneering International’s aerospace and defense work scales faster than expected, or if high margin subsea robotics holds pricing, the current overvaluation narrative could quickly look conservative.

Find out about the key risks to this Oceaneering International narrative.

Another View on Oceaneering International’s Valuation

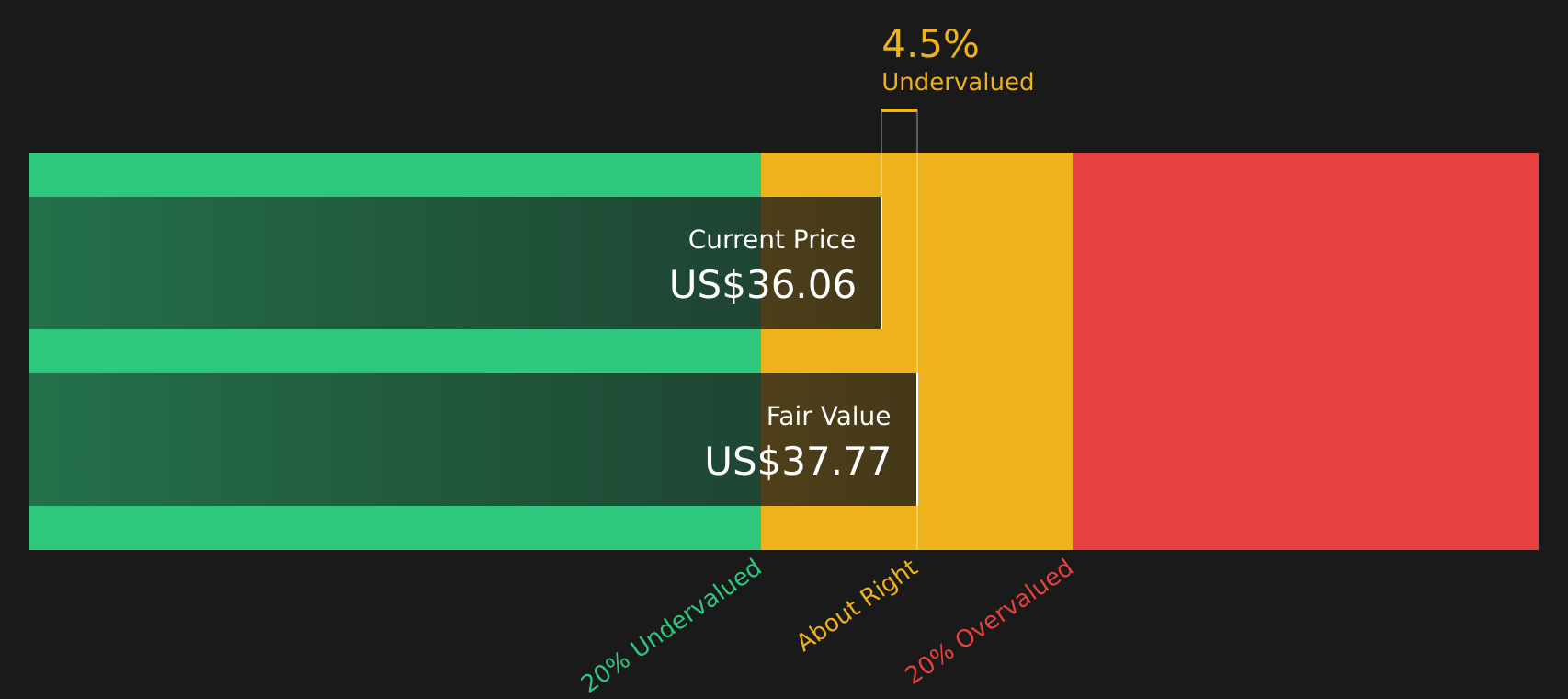

While the current fair value narrative suggests Oceaneering International is 2.3% overvalued at $36.06 versus $35.25, a separate check using our DCF model points in a different direction, with the stock trading about 4.5% below an estimated future cash flow value of $37.77. Which set of assumptions do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Oceaneering International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Oceaneering International leave you unsure, that is the point. Use the tools available to stress test the upside and downside, then weigh the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Oceaneering International?

If you are serious about building a stronger portfolio, do not stop at Oceaneering International. Use the screener to spot other opportunities before the crowd.

- Target quality at a discount by scanning companies that pass strict value and quality filters with the 45 high quality undervalued stocks

- Prioritize resilience by focusing on businesses that combine healthy balance sheets with solid fundamentals using the solid balance sheet and fundamentals stocks screener (48 results)

- Hunt for off-the-radar opportunities by reviewing the screener containing 19 high quality undiscovered gems before they become widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English