Whirlpool (WHR) Stock Could Be 31.3% Undervalued After Weak Earnings And Dividend Cut

Whirlpool (WHR) is under pressure after a weak quarter, with revenue down year on year, full year earnings guidance missing analysts’ expectations, and a costly debt refinancing leading to credit downgrades and dividend cuts.

See our latest analysis for Whirlpool.

At a share price of $38.86, Whirlpool has seen its short term momentum weaken, with the share price return down 9.4% over the past week and 25.6% over 90 days. The 1 year total shareholder return has fallen 56.7%, reflecting investor concern after weaker earnings, higher interest costs from refinancing and recent credit downgrades.

If Whirlpool's recent setbacks have you reassessing opportunities in consumer and industrial trends, this could be a useful moment to look at 31 robotics and automation stocks

With Whirlpool shares down sharply over 1 and 5 years and trading at a discount to analyst price targets and intrinsic estimates, investors now face a key question: is this genuine value, or is the market already bracing for weaker growth?

Most Popular Narrative: 31.3% Undervalued

The most followed Whirlpool narrative puts fair value at $56.55, well above the last close of $38.86, and builds a case around product mix, global footprint, and margin repair.

Introduction of over 100 new products, including space saving and multifunctional appliances (like the new KitchenAid suite and JennAir downdraft induction cooktops), addresses rising consumer demand for efficient, customizable, and premium offerings, supporting future revenue and margin growth.

Curious what sits behind a higher fair value for Whirlpool when recent returns look weak? The narrative leans heavily on projected earnings growth, modest revenue expansion, and a richer profit multiple several years out. The real story is how those ingredients are combined and discounted to arrive at that $56.55 figure.

Result: Fair Value of $56.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Whirlpool's reliance on mature markets and pressure from lower cost competitors could keep revenue growth and margins under strain, challenging that 31.3% undervalued narrative.

Find out about the key risks to this Whirlpool narrative.

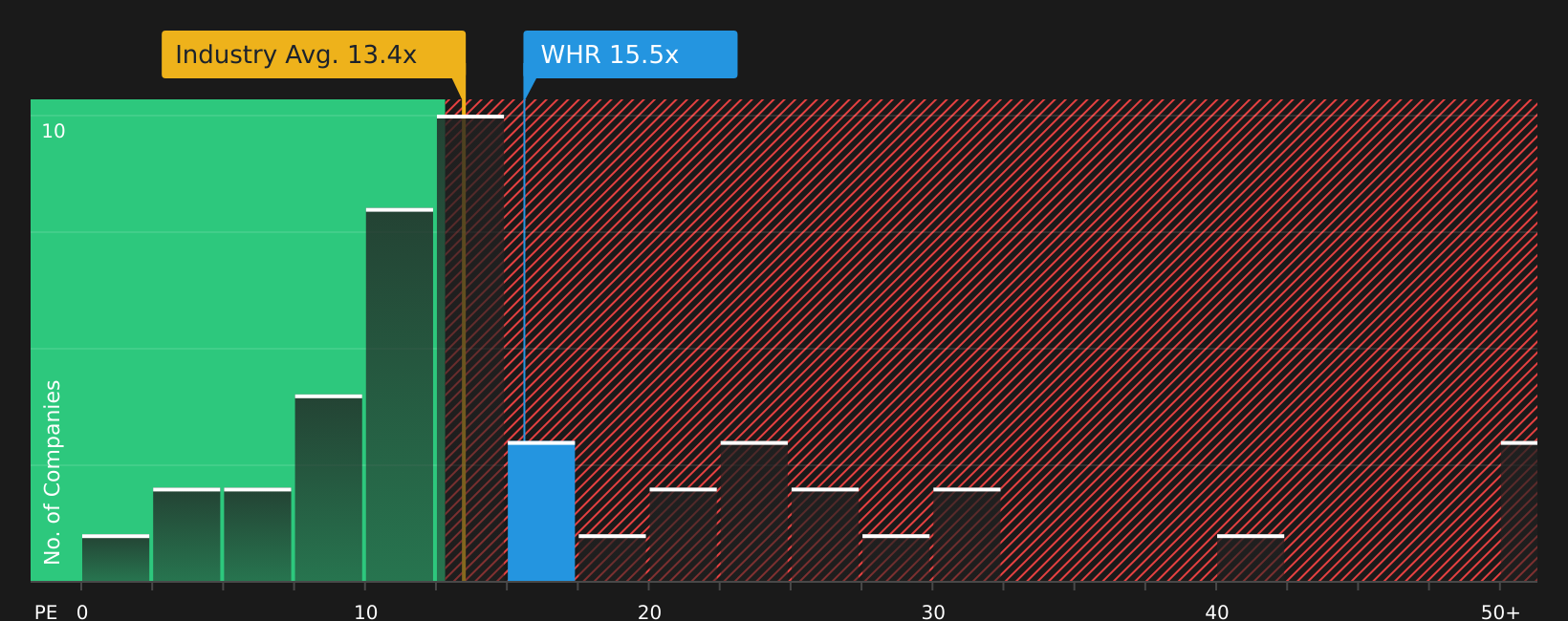

Another View: Whirlpool Through The P/E Lens

The SWS fair value model suggests Whirlpool is undervalued, yet the market is still pricing the stock at a P/E of 15.5x, above both the US Consumer Durables industry at 13.4x and peers at 14.1x, and below a fair ratio of 26.9x. It is up to you to judge whether this gap signals risk or opportunity.

To see how this valuation gap is built up from earnings and multiples, and what it could mean if the P/E moved closer to the fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Whirlpool carrying both clear concerns and some potential bright spots, it makes sense to move quickly and test the numbers against your own expectations using the 3 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Whirlpool?

Do not stop with Whirlpool. Use this moment to refresh your watchlist, compare different types of opportunities, and pressure test where your next dollar should go.

- Spot potential turnaround stories early by checking out 24 elite penny stocks with strong financials that already pair higher risk with relatively stronger financials.

- Zero in on companies that combine appealing prices with resilient fundamentals through the 45 high quality undervalued stocks before the crowd shows up.

- Prioritise capital preservation and smoother returns by reviewing 66 resilient stocks with low risk scores and see which stocks line up best with your comfort level.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English