Is Sunbelt Rentals’ Analyst Support and Ongoing Buybacks Quietly Reframing Its Capital Strategy (SUNB)?

- Earlier this week, Sunbelt Rentals Holdings Inc was previewed to report earnings of US$0.74 per share, while continuing a US$1.50 billion share repurchase program that adds stock to treasury.

- At the same time, supportive analyst opinions from firms such as Barclays, Citi and RBC Capital appear to be reinforcing confidence in the company’s ongoing buyback activity and capital deployment.

- Next, we’ll examine how this combination of upbeat analyst views and sizeable buybacks could influence Sunbelt Rentals Holdings’ investment narrative.

Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Sunbelt Rentals Holdings Investment Narrative Recap

To own Sunbelt Rentals Holdings, you generally need to believe its equipment rental platform can keep converting large project activity and specialty demand into resilient cash generation. This week’s earnings preview of US$0.74 per share and the ongoing US$1.50 billion buyback program speak most directly to the near term catalyst of earnings per share support, while the biggest current risk around project-driven utilization and margins does not appear materially altered by this news.

The most relevant recent announcement here is the detailed buyback update from March 2026, showing US$1.40 billion already deployed to repurchase about 21.9 million shares. That context helps frame today’s US$1.50 billion authorization as a continuation of an established capital return pattern, which could matter for how quickly any future earnings trajectory, whether modest or robust, feeds through to per share metrics.

Yet alongside this upbeat picture, there is still the underappreciated risk that investors should be aware of if mega project demand or utilization eventually...

Read the full narrative on Sunbelt Rentals Holdings (it's free!)

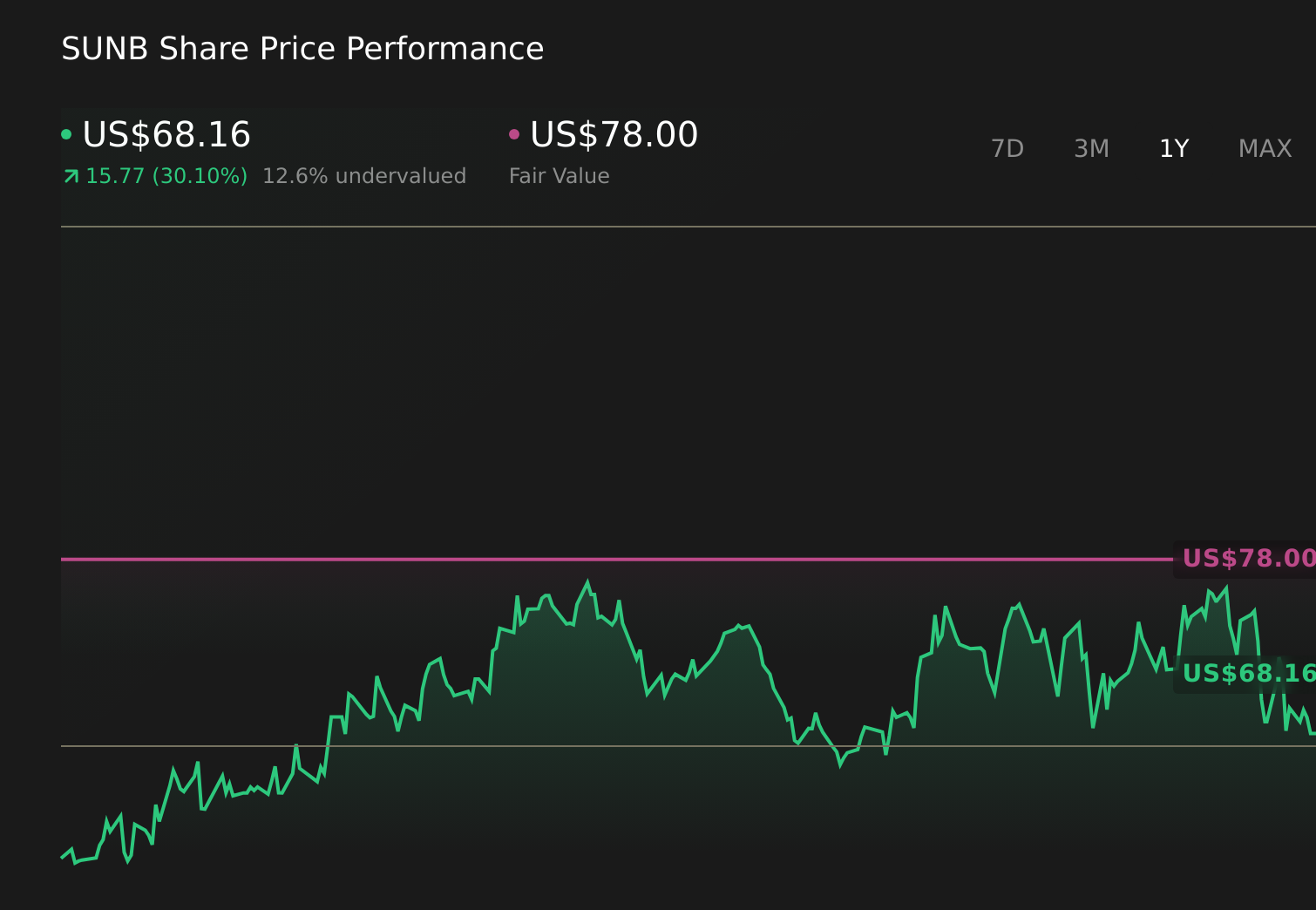

Sunbelt Rentals Holdings' narrative projects $13.4 billion revenue and $2.2 billion earnings by 2029. This requires 7.3% yearly revenue growth and about an $0.8 billion earnings increase from $1.4 billion today.

Uncover how Sunbelt Rentals Holdings' forecasts yield a $78.00 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming Sunbelt would only reach about US$12.5 billion in revenue and US$2.0 billion in earnings by 2029, which is a much more cautious story than the consensus and could look very different again once this latest earnings news and buyback progress are fully reflected.

Explore 3 other fair value estimates on Sunbelt Rentals Holdings - why the stock might be worth 6% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Sunbelt Rentals Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Sunbelt Rentals Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunbelt Rentals Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English