The Bull Case For ePlus (PLUS) Could Change Following Standout Customer Satisfaction And Partner Awards - Learn Why

- Recently, ePlus highlighted an independent VistaXM survey showing it achieved a Net Promoter Score of 74, well above typical technology industry averages, alongside being named Everpure’s Services Partner of the Year for its Storage-as-a-Service offering.

- Together, these strong customer satisfaction metrics and partner recognition underscore how ePlus’s focus on customer experience and innovative service models is resonating with its client base.

- We’ll now examine how this exceptionally high customer satisfaction, reflected in ePlus’s Net Promoter Score, may influence the company’s broader investment narrative.

Find 41 companies with promising cash flow potential yet trading below their fair value.

ePlus Investment Narrative Recap

To own ePlus, you need to believe it can turn its IT solutions, security, and AI infrastructure expertise into durable, recurring customer relationships while managing margin pressure and lumpy project-driven revenue. The new Net Promoter Score of 74 and Services Partner of the Year award reinforce the strength of its customer relationships but do not, on their own, materially change the near term risk that large, non repeatable projects and product mix could still drive earnings volatility.

The Everpure Services Partner of the Year recognition for ePlus’s Storage as a Service offering ties directly into one of the key near term catalysts: growing managed and subscription services that can smooth revenue and deepen customer stickiness. If ePlus continues to scale these types of consumption based offerings, it may gradually offset some dependence on large, one off enterprise hardware deals and support more predictable performance over time.

Yet despite strong satisfaction scores, investors should still be aware of how quickly mix shifts toward lower margin enterprise deals could...

Read the full narrative on ePlus (it's free!)

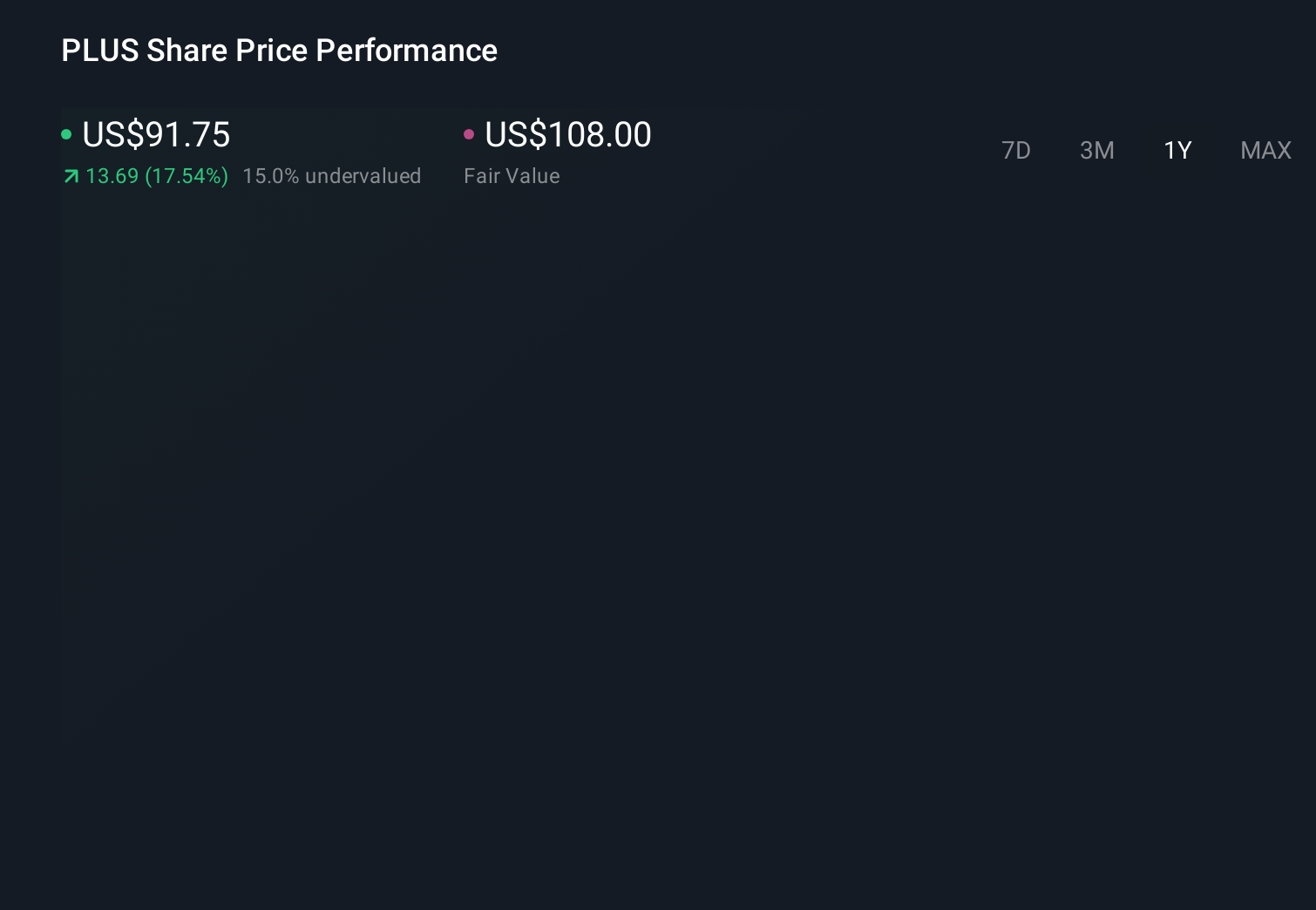

ePlus' narrative projects $2.8 billion revenue and $136.4 million earnings by 2029.

Uncover how ePlus' forecasts yield a $111.00 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$75 to US$111 per share, showing how far apart individual views can be. You should weigh that spread against the risk that ePlus’s revenue remains tied to large, project specific deals, and consider how different assumptions about that exposure can shape very different expectations for future performance.

Explore 2 other fair value estimates on ePlus - why the stock might be worth as much as 35% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your ePlus research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English