Are Want Want China Holdings Limited's (HKG:151) Fundamentals Good Enough to Warrant Buying Given The Stock's Recent Weakness?

Want Want China Holdings (HKG:151) has had a rough three months with its share price down 6.7%. However, stock prices are usually driven by a company’s financials over the long term, which in this case look pretty respectable. Particularly, we will be paying attention to Want Want China Holdings' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

Check out our latest analysis for Want Want China Holdings

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Want Want China Holdings is:

27% = CN¥4.1b ÷ CN¥15b (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. So, this means that for every HK$1 of its shareholder's investments, the company generates a profit of HK$0.27.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Want Want China Holdings' Earnings Growth And 27% ROE

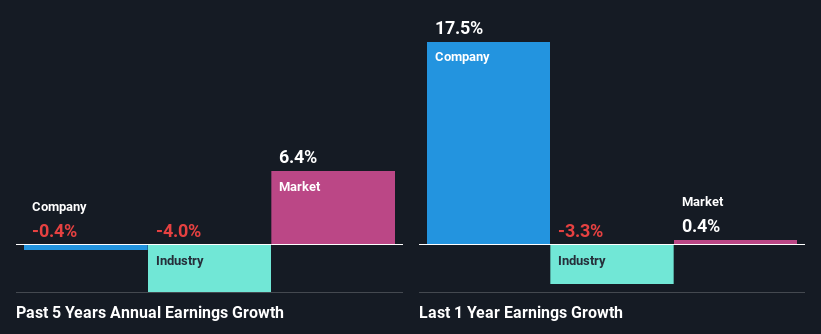

First thing first, we like that Want Want China Holdings has an impressive ROE. Additionally, the company's ROE is higher compared to the industry average of 6.0% which is quite remarkable. Despite this, Want Want China Holdings' five year net income growth was quite flat over the past five years. So, there could be some other aspects that could potentially be preventing the company from growing. These include low earnings retention or poor allocation of capital

Next, we compared Want Want China Holdings' performance against the industry and found that the industry shrunk its earnings at 4.0% in the same period, which suggests that the company's earnings have been shrinking at a slower rate than its industry, This does offer shareholders some relief

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Want Want China Holdings is trading on a high P/E or a low P/E, relative to its industry.

Is Want Want China Holdings Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 63% (meaning, the company retains only 37% of profits) for Want Want China Holdings suggests that the company's earnings growth was miniscule as a result of paying out a majority of its earnings.

In addition, Want Want China Holdings has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Looking at the current analyst consensus data, we can see that the company's future payout ratio is expected to rise to 77% over the next three years. Despite the higher expected payout ratio, the company's ROE is not expected to change by much.

Conclusion

Overall, we feel that Want Want China Holdings certainly does have some positive factors to consider. Yet, the low earnings growth is a bit concerning, especially given that the company has a high rate of return. Investors could have benefitted from the high ROE, had the company been reinvesting more of its earnings. As discussed earlier, the company is retaining a small portion of its profits. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English