Top US Growth Stocks With Insider Ownership In February 2025

As of February 2025, the U.S. stock market is experiencing a period of volatility, with the S&P 500 and Nasdaq Composite declining for four consecutive sessions due to concerns about economic uncertainty and tech sector weaknesses. In contrast, the Dow Jones Industrial Average has seen some gains, buoyed by strong performances from retail giants like Walmart and Home Depot. In this environment, growth companies with high insider ownership can offer an intriguing investment perspective as they often reflect confidence from those closest to the business operations amidst broader market fluctuations.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 25.6% |

| Super Micro Computer (NasdaqGS:SMCI) | 14.4% | 27.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.8% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Astera Labs (NasdaqGS:ALAB) | 16.1% | 61.1% |

| BBB Foods (NYSE:TBBB) | 16.5% | 41.1% |

| Clene (NasdaqCM:CLNN) | 20.7% | 59.1% |

| Enovix (NasdaqGS:ENVX) | 12.6% | 56.0% |

| Credit Acceptance (NasdaqGS:CACC) | 14.2% | 33.6% |

| Upstart Holdings (NasdaqGS:UPST) | 12.6% | 100.7% |

Let's explore several standout options from the results in the screener.

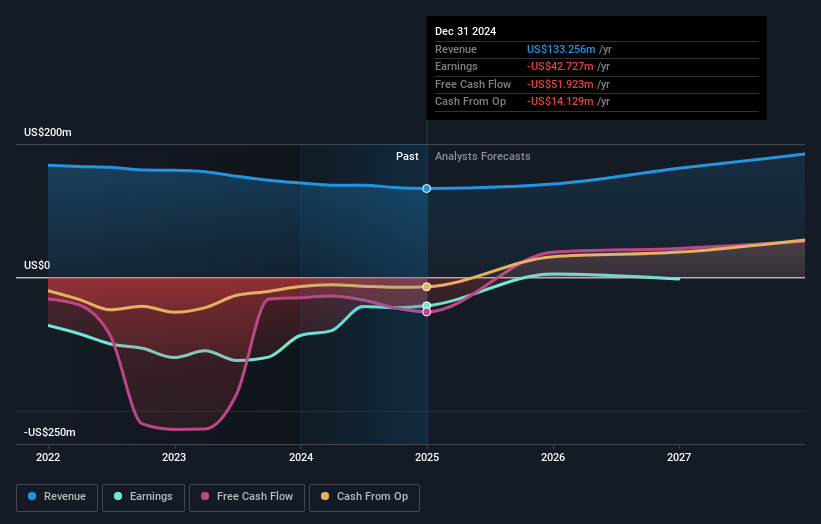

Agora (NasdaqGS:API)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Agora, Inc. operates in the real-time engagement technology sector across China, the United States, and internationally with a market cap of $515.62 million.

Operations: Agora's revenue segments are not specified in the provided text.

Insider Ownership: 24.4%

Earnings Growth Forecast: 120.3% p.a.

Agora has shown significant growth potential with earnings rising 17.3% annually over the past five years and a forecasted annual profit growth of over 120%. Despite recent revenue declines, net income improved to US$0.16 million from a previous loss. The company trades at nearly 27% below estimated fair value, suggesting potential undervaluation. Agora's buyback program repurchased almost 40% of shares, indicating strong insider confidence in its future prospects amidst anticipated profitability within three years.

- Dive into the specifics of Agora here with our thorough growth forecast report.

- Our valuation report here indicates Agora may be undervalued.

Clear Channel Outdoor Holdings (NYSE:CCO)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Clear Channel Outdoor Holdings, Inc. is an out-of-home advertising company operating in the United States, Europe, and internationally with a market cap of approximately $646.88 million.

Operations: Clear Channel Outdoor Holdings generates revenue through its out-of-home advertising operations across the United States, Europe, and other international markets.

Insider Ownership: 12.7%

Earnings Growth Forecast: 48.4% p.a.

Clear Channel Outdoor Holdings is poised for growth, with earnings projected to increase by 48.43% annually and revenue expected to outpace the US market at 22.2% per year. Despite a net loss reduction to US$179.25 million in 2024, the company trades at approximately 72.6% below its fair value estimate, indicating potential undervaluation. Recent contract extensions at major airports enhance its advertising reach, while insider ownership remains a key factor in driving future profitability expectations within three years.

- Get an in-depth perspective on Clear Channel Outdoor Holdings' performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Clear Channel Outdoor Holdings' shares may be trading at a discount.

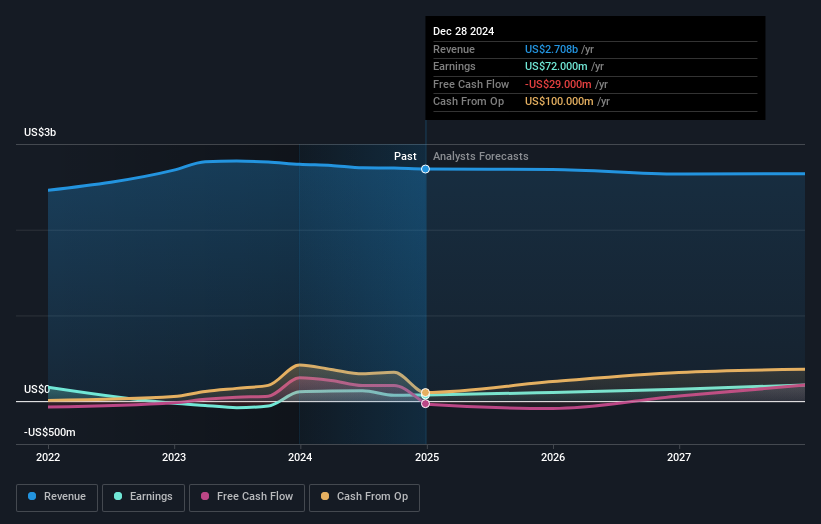

WK Kellogg Co (NYSE:KLG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: WK Kellogg Co is a food company that operates in the United States, Canada, and the Caribbean with a market cap of approximately $1.71 billion.

Operations: The company generates revenue of $2.71 billion from its manufacturing, marketing, and sales of cereal products across the United States, Canada, and the Caribbean.

Insider Ownership: 11.5%

Earnings Growth Forecast: 27.1% p.a.

WK Kellogg Co's earnings are forecast to grow significantly at 27.1% annually, outpacing the US market, despite a projected revenue decline of 0.7% per year. The company recently reported a slight drop in full-year sales to US$2.71 billion but saw an increase in quarterly net income to US$19 million. Its dividend yield of 3.15% is not well covered by free cash flows, and debt coverage by operating cash flow remains inadequate, highlighting financial challenges amidst growth prospects.

- Navigate through the intricacies of WK Kellogg Co with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that WK Kellogg Co's share price might be on the cheaper side.

Taking Advantage

- Gain an insight into the universe of 198 Fast Growing US Companies With High Insider Ownership by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English