Capital Allocation Trends At Lvji Technology Holdings (HKG:1745) Aren't Ideal

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after investigating Lvji Technology Holdings (HKG:1745), we don't think it's current trends fit the mold of a multi-bagger.

We've discovered 4 warning signs about Lvji Technology Holdings. View them for free.What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Lvji Technology Holdings, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

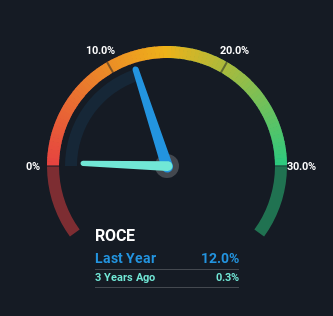

0.12 = CN¥122m ÷ (CN¥1.3b - CN¥281m) (Based on the trailing twelve months to December 2024).

Therefore, Lvji Technology Holdings has an ROCE of 12%. In absolute terms, that's a satisfactory return, but compared to the Software industry average of 5.5% it's much better.

View our latest analysis for Lvji Technology Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Lvji Technology Holdings' ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Lvji Technology Holdings.

What Can We Tell From Lvji Technology Holdings' ROCE Trend?

We weren't thrilled with the trend because Lvji Technology Holdings' ROCE has reduced by 49% over the last five years, while the business employed 52% more capital. Usually this isn't ideal, but given Lvji Technology Holdings conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. Lvji Technology Holdings probably hasn't received a full year of earnings yet from the new funds it raised, so these figures should be taken with a grain of salt.

On a side note, Lvji Technology Holdings' current liabilities have increased over the last five years to 22% of total assets, effectively distorting the ROCE to some degree. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. While the ratio isn't currently too high, it's worth keeping an eye on this because if it gets particularly high, the business could then face some new elements of risk.

The Bottom Line

We're a bit apprehensive about Lvji Technology Holdings because despite more capital being deployed in the business, returns on that capital and sales have both fallen. This could explain why the stock has sunk a total of 76% in the last five years. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

Lvji Technology Holdings does have some risks, we noticed 4 warning signs (and 1 which can't be ignored) we think you should know about.

While Lvji Technology Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English