Earnings Release: Here's Why Analysts Cut Their BRC Inc. (NYSE:BRCC) Price Target To US$2.83

Shareholders in BRC Inc. (NYSE:BRCC) had a terrible week, as shares crashed 30% to US$1.57 in the week since its latest quarterly results. Revenues of US$90m beat expectations by a respectable 2.2%, although statutory losses per share increased. BRC lost US$0.04, which was 50% more than what the analysts had included in their models. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

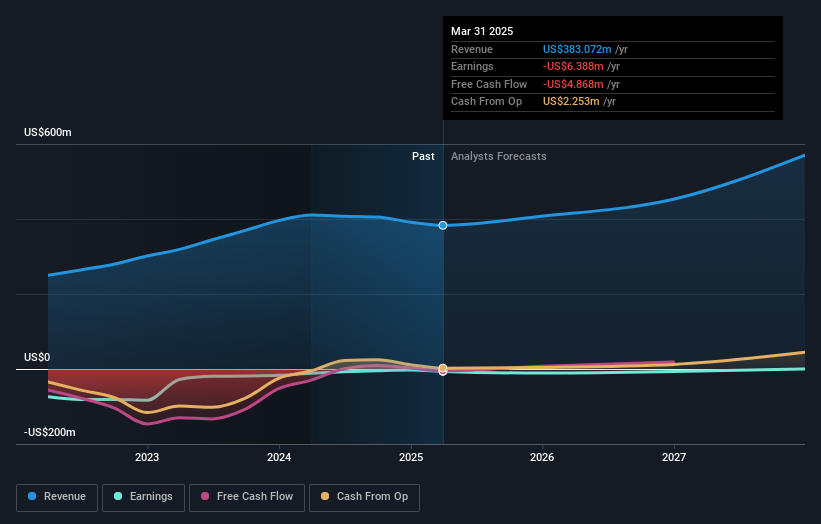

Following the latest results, BRC's five analysts are now forecasting revenues of US$407.4m in 2025. This would be a reasonable 6.4% improvement in revenue compared to the last 12 months. Losses are predicted to fall substantially, shrinking 30% to US$0.057. Before this latest report, the consensus had been expecting revenues of US$406.5m and US$0.04 per share in losses. So it's pretty clear the analysts have mixed opinions on BRC even after this update; although they reconfirmed their revenue numbers, it came at the cost of a massive increase in per-share losses.

See our latest analysis for BRC

With the increase in forecast losses for next year, it's perhaps no surprise to see that the average price target dipped 11% to US$2.83, with the analysts signalling that growing losses would be a definite concern. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on BRC, with the most bullish analyst valuing it at US$4.00 and the most bearish at US$2.00 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that BRC's revenue growth is expected to slow, with the forecast 8.6% annualised growth rate until the end of 2025 being well below the historical 16% p.a. growth over the last three years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 2.4% per year. So it's pretty clear that, while BRC's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at BRC. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple BRC analysts - going out to 2027, and you can see them free on our platform here.

Plus, you should also learn about the 1 warning sign we've spotted with BRC .

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English